")

Important Keyword: Capital Gains Exemption, Sale of Property, Section 54EC.

Table of Contents

Section 54EC of Income Tax Act

When contemplating the sale of a long-term capital asset such as land or a building, the prospect of generating income can be gratifying. However, it’s imperative to recognize that this decision entails the responsibility of fulfilling capital gains tax obligations as mandated by the income tax department. Whether it involves the sale of land, a building, or both, it’s necessary to compute the capital gains and settle the corresponding tax liabilities. Thankfully, in the scenario of transferring a long-term asset, there exists a prospect for capital gain exemption through investment in Bonds under section 54EC of the Income Tax Act.

What is Section 54EC?

Section 54EC of the Income Tax Act offers a capital gain exemption opportunity to taxpayers who are divesting their long-term capital assets, such as land, buildings, or both. This provision allows them to reinvest the capital gains amount into specific bonds issued by the Government of India, thereby enabling tax savings. The designated bonds issued by the Government of India include those issued by the National Highway Authority of India (NHAI), Rural Electrification Corp. Ltd. (REC), Power Finance Corporation (PFC), and Indian Railways Finance Corporation (IRFC).

Who can claim an exemption under Section 54EC of Income Tax Act?

To claim an exemption under Section 54EC of the Income Tax Act, taxpayers must meet specific criteria:

- Eligibility: Any taxpayer, including individuals, Hindu Undivided Families (HUFs), companies, LLPs, and firms, can avail of this exemption.

- Nature of Asset: The asset being sold must qualify as a Long Term Capital Asset (LTCA), such as land or buildings, which the taxpayer has held for a minimum of 24 months before the sale.

- Investment Timeline: The taxpayer must invest the capital gains amount into specified bonds within 6 months from the date of the transfer of the asset.

- Approved Bonds: The investment must be made in bonds issued by entities like the National Highways Authority of India (NHAI), Rural Electrification Corporation (REC), or any other bonds notified by the Central Government.

- Investment Limit: The investment amount cannot exceed INR 50 lakhs during the current financial year and the succeeding financial year.

By adhering to these conditions, taxpayers can benefit from the capital gains exemption provided under Section 54EC, thereby reducing their tax liability while contributing to infrastructure development through bond investments.

What is the amount of exemption available under Section 54EC of Income Tax Act?

As highlighted earlier, the exemption amount under Section 54EC is determined by the lesser of two factors: the cost of NHAI/REC Bonds or the capital gains from the sale of land or building.

For instance, let’s consider Jay’s scenario in the financial year 2023-24. Jay sold a piece of land for INR 60,00,000, which he had originally purchased in the financial year 2018-19 for INR 30,00,000. Subsequently, in the same financial year, Jay invested INR 45,00,000 in NHAI bonds.

In this case, Jay can claim an exemption under Section 54EC as follows:

The cost of NHAI bonds: INR 45,00,000 Capital gains from the sale of land: INR 60,00,000 – INR 30,00,000 = INR 30,00,000 Since the lower of the two amounts is INR 30,00,000, Jay can claim this as the exemption under Section 54EC while filing his income tax return for the financial year 2023-24. This provision offers taxpayers a means to mitigate their tax liability by investing in specified bonds, contributing to their financial planning strategy.

| Particulars | Amount (INR) |

| Sales Consideration | 60,00,000 |

| Less: Indexed cost of acquisition (30,00,000*348/280) | (37,28,571) |

| Long Term Capital Gain | 22,71,429 |

| Investment in NHAI Bonds | 45,00,000 |

| Section 54EC Exemption amount | 22,71,429 |

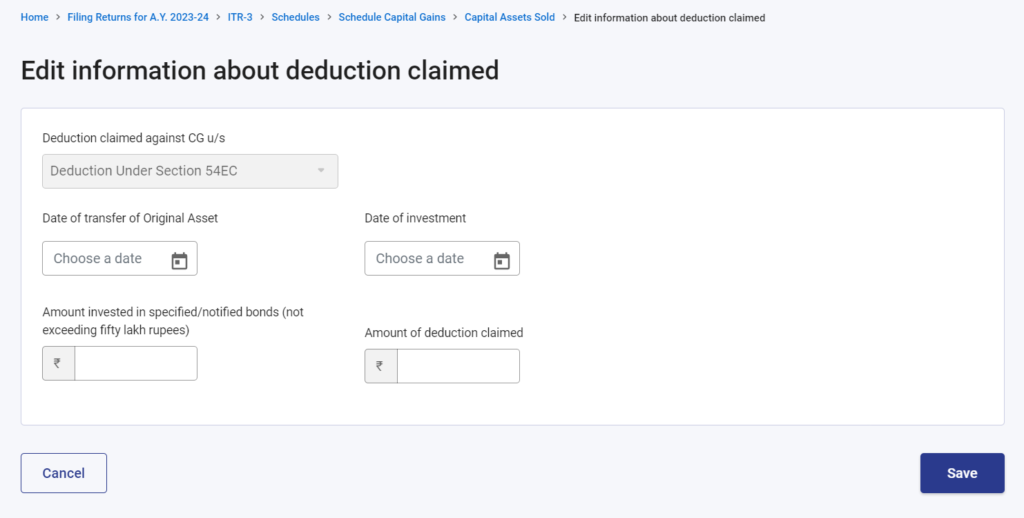

Reporting of Section 54EC in ITR

When reporting income from capital gains in their Income Tax Return (ITR), taxpayers have specific forms designated for this purpose, namely ITR-2 and ITR-3. Within these forms, taxpayers must navigate to Schedule CG to provide details of their capital gains from the sale of assets such as land, buildings, or both.

Moreover, if a taxpayer is claiming an exemption under section 54EC, they must ensure to include this information accurately in their ITR. The process involves entering the relevant details in the appropriate sections of the form as follows:

- Schedule CG: Taxpayers should provide comprehensive information regarding their capital gains, including details of the assets sold, the consideration received, and the cost of acquisition.

- Exemption under Section 54EC: If the taxpayer has invested the capital gains amount in specified bonds under section 54EC to claim exemption, they must report this in their ITR. This typically involves entering the relevant details of the investment, such as the amount invested, the type of bonds, and other pertinent information.

What happens to exemption if the taxpayer sells the 54EC Bonds?

If a taxpayer claims an exemption under Section 54EC of the Income Tax Act and sells the bond within a lock-in period of 5 years, different tax implications can arise:

Situation 1: If the taxpayer sells the bond within 5 years from the date of purchase:

Consequences: The exemption under Section 54EC is revoked. The amount of exemption previously claimed by the taxpayer will be deducted from the cost of the asset. Consequently, the Capital Gains will be calculated as the total sales value minus the adjusted cost of the asset.

Situation 2: If the taxpayer sells the bond after 5 years from the date of purchase:

Consequences: In this scenario, the exemption under Section 54EC remains intact. The taxpayer will still be eligible to claim the index cost of acquisition while computing Capital Gains on the bonds sold.

Understanding these distinctions is crucial for taxpayers to accurately assess their tax liabilities and plan their financial transactions effectively within the framework of the Income Tax Act.

Read More: Section 54B of Income Tax Act: Capital Gains Exemption on Sale of Agricultural Land

Web Stories: Section 54B of Income Tax Act: Capital Gains Exemption on Sale of Agricultural Land

Official Income Tax Return filing website: https://incometaxindia.gov.in/

FORM GST INS -01: AUTHORISATION FOR INSPECTION OR SEARCH

Circular No. 223/17/2024-GST: Amendment in circular no. 1/1//2017 in respect of Proper officer for provisions relating to Registration and Composition levy under the Central Goods and Services Tax Act, 2017 or the rules made thereunder.

FORM GST ITC-04: Details of goods/capital goods sent to job worker and received back

0 Comments