Important Keyword: Income Tax, IT Notice, Notice u/s 142(1).

Table of Contents

Section 142(1): Inquiry Before Assessment

Section 142(1) notices are issued by the Income Tax Department for various reasons, including non-filing of returns, discrepancies in tax returns, incomplete information, underreported income, suspicions of tax evasion, reassessment, and statute of limitations. These notices serve as a means for the department to request additional information or clarification regarding the disclosures made in the tax returns.

Purpose of Notice under section 142(1) of Income Tax Act

Section 142(1) of the Income Tax Act empowers the Income Tax Department to issue notices for various purposes, primarily to ensure compliance and accuracy in tax filings. Let’s delve into these purposes in a simplified manner:

Filing of Income Tax Return: If an individual or entity fails to file their income tax return within the stipulated time frame or by the end of the relevant assessment year, the Income Tax Department may issue a notice under section 142(1) prompting them to do so. It’s crucial to note that merely filing the return isn’t sufficient; it must also be electronically verified within 30 days to avoid it being deemed invalid.

Submission of Specific Documents: Even after filing the return, the Assessing Officer (AO) may require the taxpayer to furnish specific accounts and documents to validate the information provided. These could include evidence supporting claimed deductions, invoices related to business expenses, or any other documents deemed necessary for assessment.

Additional Information as Required: The AO reserves the right to seek additional information, notes, or workings from the taxpayer pertaining to specific aspects of their financial affairs. This could include details on assets and liabilities or any other relevant information essential for a thorough assessment.

Receiving a notice under section 142(1) is not uncommon and doesn’t necessarily indicate wrongdoing. It’s primarily a means for the tax authorities to ensure accuracy and completeness in tax filings, thereby fostering transparency and compliance within the tax system.

Sample Notice under section 142(1) of Income Tax Act

Consequences of non-compliance

When a taxpayer receives a notice under section 142(1), it’s imperative to respond promptly. Ignoring such notices can lead to serious consequences, including:

Best Judgment Assessment under section 144: If the taxpayer fails to respond, the assessing officer may resort to Best Judgment Assessment, wherein the officer assesses the taxpayer’s income to the best of their judgment based on available information.

Penalty Imposition of ₹10,000: Non-compliance with the notice may result in the imposition of a penalty of ₹10,000.

Warrant for Search under section 132: In severe cases of non-compliance, the Income Tax Department may issue a warrant for a search operation under section 132 to gather necessary information.

Possibility of Imprisonment: Failure to comply with the notice can also lead to imprisonment for up to 1 year, with or without a fine.

To streamline the assessment process and ensure transparency, the Income Tax Department has introduced E-assessment through the ‘Faceless Assessment Scheme, 2019’. Under this scheme, assessments are conducted in a faceless manner, with exceptions. If the assessing officer remains unsatisfied with the response to the notice issued under section 142(1), they may proceed with scrutiny assessment under this scheme.

Responding to the notice can be done online through the following steps:

Log in to the Income Tax e-filing portal.

Select “Pending Action” and then “E-Proceeding”.

Choose “View Notices” and select the notice for which a response is required.

Submit a response by clicking on “Select Response type for Notice” and choose between Partial Response or Full Response as per the requirement.

Adhering to these steps ensures timely and accurate responses to notices issued under section 142(1), thereby avoiding any potential penalties or legal repercussions.

Important Keyword: Income Tax, IT Notice, Section 143(2).

Table of Contents

Section 143(2): Notice for Scrutiny Assessment

After a taxpayer files their income tax return, the Income Tax Department initiates the review and assessment process. This involves carefully examining the returns to ensure accuracy and authenticity. If there are any discrepancies or additional information is required, the department can issue various notices such as Notice under section 143(1)(a) or Notice under section 142(1), among others.

Failure to respond to these notices or to provide the requested information may lead to further assessment procedures. One such procedure is known as scrutiny assessment, which is initiated when the department issues a notice to scrutinize the return under section of the Income Tax Act. This allows the department to conduct a more detailed examination of the taxpayer’s income and deductions to ensure compliance with tax laws.

Why Notice under section 143(2) is issued?

Under Section 143(2) of the Income Tax Act, the department issues formal notices to conduct scrutiny assessments, typically under Section 143(3).

Scrutiny assessment, or detailed assessment under Section 143(3), involves verifying the accuracy and genuineness of various claims and deductions made in Income Tax Returns. The aim is to ensure that the taxpayer has accurately reported their income and deductions and paid the corresponding taxes.

There are three types of notices under Section 143(2):

Limited Scrutiny: Cases are selected based on specific parameters, often through Computer-Assisted Scrutiny Selection (CASS). This scrutiny focuses on particular areas mentioned in the notice, such as discrepancies in tax credits or property sales.

Complete Scrutiny: A thorough review is conducted of the filed ITR and supporting documents. While cases are still identified through CASS, this scrutiny is not limited to specific areas. However, the assessing officer can only inspect documents relevant to the specific assessment year.

Manual Scrutiny: Cases for manual scrutiny are selected based on criteria defined by the Central Board of Direct Taxes (CBDT). These criteria may change annually and aim to ensure comprehensive examination of relevant cases.

Sample Notice u/s 143(2)

Under Section 143(2) of the Income Tax Act, the notice must be issued within 3 months from the end of the financial year in which the return of income is filed. For example, if a taxpayer files their return for the financial year 2022-23 on July 25, 2023, the AO can issue a notice under Section 143(2) until June 30, 2024, which is three months from the end of FY 2023-24.

Upon receiving the notice, the taxpayer must respond by submitting the necessary documents online or appearing before the AO to provide arguments and evidence.

The AO will then proceed to issue an assessment order after examining the submitted documents. The time period to issue a final assessment order under Section 143(3) is 9 months from the end of the relevant Assessment Year.

Non-compliance with the notice can lead to penalties under Section 272A, amounting to ₹10,000 for each failure. Additionally, the AO may conduct a best judgment assessment under Section 144 and, if the taxpayer is found guilty, imprisonment may be imposed.

Important Keyword: Income Tax, IT Notice, Notice u/s 148.

Table of Contents

Section 148: Income Escaping Assessment

The taxes paid by individuals are vital for funding public services. However, there are instances where taxpayers might either intentionally or unintentionally fail to report certain portions of their income when filing their taxes. In response to this, tax authorities conduct thorough examinations to ensure accurate reporting of all income sources. In such situations, the Assessing Officer issues a notice under Section 148 for ‘Income Escapement Assessment’. The objective of this assessment is to uncover any concealed income, whether it was intentionally hidden or overlooked due to inadvertence.

Section 148 of the Income Tax Act

If upon reviewing the filed return, the Assessing Officer (AO) harbors doubts regarding the completeness of income disclosure by the taxpayer, they can initiate further assessment proceedings by issuing a notice under section 148.

In accordance with the Finance Act 2022, section 148A was introduced. In compliance with this section, the AO must conduct an inquiry and grant the taxpayer an opportunity to present their explanation before issuing a notice under section 148. The taxpayer must be allowed to provide their explanation within a timeframe of 7 days, which can be extended for up to 30 days.

The issuance of a Notice under Section 148 is subject to various conditions and terms as follows:

The AO must have a valid reason to believe that taxable income has escaped assessment, supported by substantial evidence. Mere suspicion without evidence cannot be the basis for such a notice.

The AO must provide the reasons in writing before issuing the notice under section 148. A mere change of opinion cannot constitute a reason to believe.

The AO cannot issue a notice based on information provided by the taxpayer during the assessment.

The AO can only issue a notice if they have received new information and not discovered it themselves by reading.

The AO can issue a notice if previously disclosed relevant information comes to notice, even at a later time.

Furthermore, notice under section 148 can only be issued if the following conditions are satisfied:

The taxpayer failed to file the return in response to the notice under section 142.

The taxpayer filed the return under Section 139.

The taxpayer is providing complete and accurate information for completing the assessment of the relevant Assessment Year.

The time limit for issuing a notice for income escaping assessment is provided under section 149 of the Income Tax Act. According to Section 149:

The notice can be issued within 4 years from the end of the relevant assessment year.

The AO can issue a notice up to 10 years from the end of the relevant assessment year if specific conditions are met.

A notice for income escaping assessment related to assets located outside India can be issued within 16 years from the end of the relevant Assessment Year.

As for who can issue a notice under Section 148:

An AO above the rank of Assistant Commissioner or Deputy Commissioner can issue a notice, provided the Joint Commissioner is convinced, with recorded justifications, that it is an appropriate case.

The AO cannot issue a notice after 4 years from the end of the relevant assessment year, but higher authorities can issue it even after this period if valid reasons are found.

Regarding replying to the notice under Section 148:

Upon receiving the notice, the taxpayer should review the recorded reasons for issuing the notice. If these reasons are not provided, the taxpayer must request the AO to furnish a copy of the recorded reasons.

If the taxpayer agrees with the reasons given by the AO, they must respond within the stipulated time frame by either filing the requested return or providing the documents and information as requested.

The taxpayer can dispute the validity of the notice before the AO or higher authorities if the notice is found to be invalid or if the reasons for initiating the assessment under section 147 are deemed inadequate.

If the authority’s decision favors the taxpayer, assessment procedures can be suspended. However, if the authorities rule against the taxpayer, the AO can proceed with the reassessment.

Consequences of not responding to notice

In cases where a taxpayer fails to respond to the notice issued under section 148, the Assessing Officer (AO) has the authority to conduct the assessment based on the available information. This means they can estimate the taxpayer’s income and assess it to the best of their judgment under section 144 of the Income Tax Act.

If taxpayers disagree with the assessment made by the AO, they have the option to file an appeal. The appeal can be filed with either the Commissioner of Income Tax (Appeals) or the Income Tax Appellate Tribunal (ITAT). These are the next levels of authority where taxpayers can contest the assessment and present their case for review.

Important Keyword: Income Tax, IT Notice, Notice under Section 156.

Table of Contents

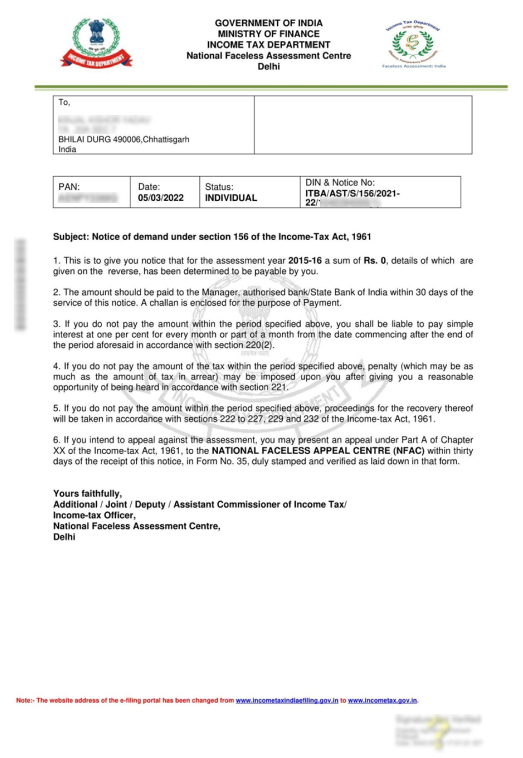

Section 156: Notice of Demand

After the completion of the assessment or re-assessment process, the Income Tax Department undertakes the crucial task of evaluating whether any additional tax liability is owed by the taxpayer. If such an outstanding liability exists, the department initiates the process by issuing a demand notice as per section 156 of the Income Tax Act. This notice serves to inform the taxpayer of the total amount due, comprising of various components such as interest, penalties, fines, and any other applicable charges. Additionally, the notice stipulates a specific timeframe within which the taxpayer is required to settle the outstanding amount.

Notice for Outstanding Demand under Section 156?

When an order is issued under the provisions of the Income Tax Act, and it entails an outstanding liability, the Income Tax Department issues a notice under section 156 to the taxpayer. This notice encompasses demands related to various sections of the Act, such as section 143(1), 200A(1), 206CB(1), among others. Any notice specifying a sum payable under these sections is regarded as a Demand Notice under section 156. The taxpayer is obligated to remit the specified amount within 30 days of receiving the notice.

Sample Notice under section 156

How to Respond to Outstanding Tax Demand Notice?

For submitting a response to outstanding demand, the taxpayer can follow below-mentioned steps:

Log in to the e-Filing Portal Log in to the e-Filing portal. Navigate to Pending Actions > Response to Outstanding Demand to view a list of your outstanding demands from the dashboard.

If you agree pay the demand amounts before submitting a response. Click on Pay Now to make payment of outstanding demand.

Submit Response If the taxpayer has not paid the demand or disagrees with the demand then they can submit their response accordingly.

Further, the taxpayer has the following options available for submitting a response to the demand notice issued u/s 156.

Agree with demand.

Fully disagree with demand.

Partially disagree with demand.

Option 1: Agree with Demand

Part A- Demand is correct but payment is pending. If you agree with the demand notice, you can select the Demand is Correct option. Moreover, you get an opportunity to pay the dues from here only by selecting Not Paid Yet option. Once the payment is done, the response to the demand will be submitted automatically.

Part B: The demand is correct and amounts are already paid. On the Response to Outstanding Amount page, select the Demand is Correct option and the disclaimer. Then click on the checkbox with Yes, Already paid and Challan has CIN, and Click on Add Challan Details.

Here, input the challan details. After entering the details, upload a copy of the challan (PDF). Once you save the challan details, the system will display a success message along with the transaction ID on the next tab.

Option 2: Fully Disagree with demand.

If you disagree with the demand notice, select Disagree with the demand (Either in full or in part) option and click on Add Reasons.

Then, select the reason(s) for your disagreement from the options and click Apply. (You can select one or more options)

After selecting the appropriate reasons for your disagreement, select each reason you listed on the Response to Outstanding Amount page and enter the appropriate explanation for disagrrement. Once the explanation is saved, submit the response.

Option 3: Partially disagree with Demand.

If a taxpayer believes that the outstanding demand is only partially correct, they have the option to submit reasons for their disagreement. In such cases, the taxpayer is required to make payment for the portion of the amount with which they agree. Once the payment is successfully made, the system will prompt the taxpayer to proceed to the Response to Outstanding Amount page. Here, they can submit their response. Upon successful submission, the system will display a confirmation message along with a Transaction ID.

Time Limit to Respond

The taxpayer must settle the outstanding demand within 30 days from the date of service of the notice. However, in certain instances, the assessing officers may reduce this period to 30 days if they deem it detrimental for the department to allow a longer period for payment, with prior approval from the joint commissioner.

Furthermore, taxpayers can apply for an extension of the payment period or request to make payments in installments. However, such applications must be made before the end of the initial 30-day period.

Consequences of Delay

Interest under section 220(2): Interest is levied at a rate of 1% per month or part of the month after the expiration of the initial 30-day period. This interest is payable by the taxpayer, even if the assessing officer has approved an extension of the payment period.

Penalty under section 221: The assessing officer has the authority to impose a penalty of up to the amount of the demand specified in the outstanding demand notice. However, the taxpayer must be given a reasonable opportunity to be heard. If the taxpayer can demonstrate that the default occurred due to genuine reasons, no penalty will be imposed.

Important Keyword: E-Compliance Portal, Income Tax Return, Income Tax Website, IT Notice.

Table of Contents

Submit Response on E-Compliance Portal

In India, meeting income tax return deadlines is crucial to stay compliant with the law. Let’s simplify the key dates and consequences to ensure you’re on track with your tax obligations.

1. Original Income Tax Return (ITR) Filing Deadline:

For individuals not subject to tax audit: The deadline is July 31st following the end of the financial year.

For those undergoing tax audit: The deadline extends to September 30th after the financial year concludes.

2. Belated or Revised Return Filing Deadline:

If you miss the original deadline, you can file a belated return under Section 139(4) or a revised return under Section 139(5) until March 31st of the subsequent year.

Consequences of Missing Deadlines:

Failure to file by the due date leads to notifications from the Income Tax Department. They may reach out via email or SMS to remind non-filers about their obligations.

In the financial year 2018-19 (Assessment Year 2019-20), the Income Tax Department sent SMS alerts to numerous taxpayers who hadn’t filed their returns.

Remember, timely filing not only avoids penalties but also ensures you’re fulfilling your legal duties. Stay informed and meet your tax deadlines to enjoy a hassle-free tax season. If you have any doubts, consult a tax professional for guidance.

The Income Tax Department employs a sophisticated system called the Non-Filers Monitoring System (NMS) to track taxpayers who have not filed their income tax returns. Here’s a simplified breakdown of how it works:

1. Data Collection:

The ITD gathers information on taxpayers’ financial activities from various sources, including:

Annual Information Return (AIR)

Central Information Branch (CIB) data

Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) returns.

2. Analysis and Identification:

Using advanced algorithms, the ITD analyzes this data to identify individuals who should have filed income tax returns but haven’t.

3. Notice Issuance:

Based on the findings, the ITD issues notices to non-filers, notifying them of their potential tax liability.

These notices serve as reminders to taxpayers to fulfill their tax obligations and file their returns promptly.

Annual Information Return(AIR)

The Annual Information Return (AIR) serves as a vital tool for the Income Tax Department to monitor high-value transactions made by individuals and Hindu Undivided Families (HUFs). Let’s delve into its significance and the actions taken by the ITD for non-filers:

1. Reporting High-Value Transactions:

AIR requires specified entities to report various high-value transactions to the income tax department. These include cash deposits, credit card bills, mutual fund investments, purchase of immovable property, and more, surpassing specific thresholds.

2. Example Transactions Reported:

AIR-001: Cash deposits exceeding Rs. 10,00,000 in a savings bank account.

AIR-002: Credit card bills amounting to Rs. 2,00,000 or more.

AIR-003: Mutual fund investments totaling Rs. 2,00,000 or above, and so on.

3. Impact on Non-Filers:

For taxpayers who haven’t filed their income tax returns but have significant financial transactions reflected on the e-Compliance Portal, the ITD takes proactive measures:

Sending SMS alerts to remind them of their obligation to file returns.

Initiating queries to verify the information available on the e-Compliance Portal, ensuring accuracy and compliance.

Action to be taken for Income Tax Non-Filing Notice

If you’ve received a notice for non-filing of your income tax return via SMS, it’s essential to take prompt action. Here’s a straightforward guide on what to do:

1. File Income Tax Return or Submit Response:

a. Log in to your account on incometaxindiaefiling.gov.in. b. Navigate to Compliance > Compliance Portal. c. Click on e-Campaign. d. Under “e-Campaign – Non-Filing of Return,” select the relevant Financial Year. e. Choose “e-Campaign – Response on Filing of Income Tax Return” for the same Financial Year. f. From the dropdown menu, select your response and reason for non-filing. Specify the mode of filing. g. Provide the Date, Acknowledgement Number, and any Remarks. h. Click on Submit.

2. Confirm Information Provided:

a. Log in to your account on incometaxindiaefiling.gov.in. b. Visit Compliance > Compliance Portal. c. Click on e-Campaign. d. Select “e-Campaign – Non-Filing of Return” for the applicable Financial Year. e. Under “e-Campaign – Information Confirmation,” choose the same Financial Year. f. Click on the tab to view transactions and validate the information provided.

By following these steps diligently, you can respond to the non-filing notice efficiently and ensure compliance with income tax regulations. It’s crucial to stay proactive and address such notices promptly to avoid any potential penalties or further inquiries from the Income Tax Department.