")

Important Keyword: Income from salary, Income Tax, Relief 89(1), Salary Arrears.

Table of Contents

Arrears of Salary- Taxability & Relief under Section 89(1)

Arrears of salary refer to the amount of salary from a previous period that is received by an employee during the current year. This can occur due to various reasons such as a retrospective revision in the employee’s salary or the release of disputed salary by the employer at a later date.

Imagine this scenario: You’ve been working diligently at your job, and suddenly you receive a lump sum payment that includes salary owed to you from previous months or years. This sudden windfall is what’s known as arrears of salary. It’s essentially the backlog of payments that you should have received earlier but are being paid to you now.

Arrears of salary can arise due to a variety of situations. For instance, if there’s a dispute over your salary or if there’s a retrospective change in your pay structure, you may receive arrears of salary to make up for the shortfall in previous payments. It’s like catching up on missed payments from the past.

What are arrears of Salary?

Arrears of salary occur when an employee receives payment for work done in a previous period but received in a different assessment year. This can happen due to various reasons, such as delayed salary increments or retroactive revisions to salary agreements. Employers typically list these arrears separately in salary slips and in Part B of Form 16, ensuring transparency in financial records.

When it comes to taxation, arrears of salary are considered part of the individual’s total income for the year in which they are received. While this may lead to concerns about being taxed at a higher rate, especially if it pushes the taxpayer into a higher tax bracket or changes the applicable slab rate, relief is available under Section 89(1) of the Income Tax Act.

Let’s illustrate this with an example:

Arjun’s monthly salary is INR 50,000, but his employer raises it to INR 60,000 per month from April 2020, with effect from March 2020. Since Arjun has already received his March 2020 salary at the previous rate, the additional INR 10,000 for that month is paid to him in April 2020. This additional payment constitutes Arjun’s salary arrears.

Relief under Section 89(1)

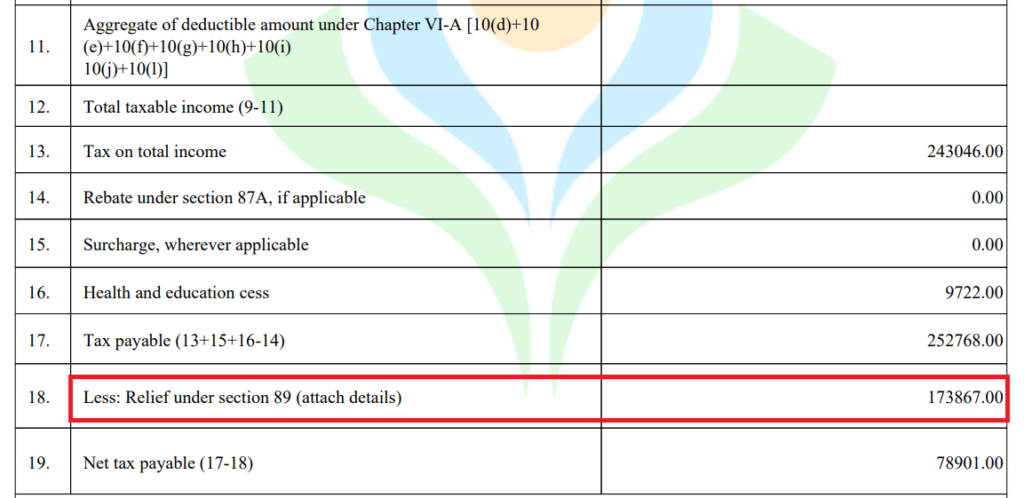

When a taxpayer receives salary arrears or advances, or profits in place of salary, relief can be sought under Section 89(1) of the Income Tax Act. This provision is designed to prevent individuals from facing higher tax liabilities due to variations in tax slab rates between different financial years.

If an individual’s total income includes past salary payments made in the current financial year, and if the tax rates differed in the years when the income was earned and when it was received, it could result in increased tax liabilities. To address this, Section 89(1) offers relief to taxpayers, ensuring they are not unfairly burdened with additional taxes.

Employers typically calculate this relief under Section 89(1) and include it in Part B of Form 16. Additionally, taxpayers can claim relief by filing Form 10E on the income tax website. This process ensures that individuals receive the appropriate tax relief and are not unduly taxed on income received in previous years.

File Form 10E

Calculation of tax relief under Section 89(1) is crucial for individuals receiving salary arrears or advances, ensuring they are not unfairly taxed due to variations in income across financial years. Let’s illustrate this process through an example:

Consider Arjun, whose salary was INR 4,80,000 (40,000 per month) for FY 2019-20. His employer increased his salary to INR 7,80,000 (65,000 per month) in April 2020, effective from March 2020. Consequently, the arrears for March 2020 amount to INR 25,000.

- Tax liability on total income including arrears for the year of receipt (FY 2020-21): Total Income (including arrears): INR 8,05,000 Tax Liability: INR 76,440

- Tax liability on total income excluding arrears for the year of receipt (FY 2020-21): Total Income (excluding arrears): INR 7,80,000 Tax Liability: INR 71,240

- Difference in tax liability between step 1 and step 2: Difference: INR 5,200

- Tax liability on total income excluding arrears for the year of accrual (FY 2019-20): Total Income (excluding arrears): INR 4,80,000 Tax Liability: NIL

- Tax liability on total income including arrears for the year of accrual (FY 2019-20): Total Income (including arrears): INR 5,05,000 Tax Liability: INR 14,040

- Difference in tax liability between step 4 and step 5: Difference: INR 14,040

- Relief under Section 89(1): Tax Relief = Step 3 – Step 6 Tax Relief = INR 5,200 – INR 14,040 = NIL

It’s essential to note that the above calculation is based on the old tax regime. Taxpayers can also use the Income Tax Department’s calculator for Relief under Section 89(1) to compute tax relief accurately.

Furthermore, taxpayers should ensure they file Form 10E to claim relief under Section 89(1) to avoid receiving an income tax notice from the tax department. This form is mandatory from the financial year 2014-15 onwards and is necessary for individuals seeking relief under Section 89(1).

Read More: Rent Free Accommodation ( RFA )

Web Stories: Rent Free Accommodation ( RFA )

Official Income Tax Return filing website: https://incometaxindia.gov.in/

0 Comments