")

Important Keyword: Form 16, Form 16A, Form 16B, TDS Certificate.

Table of Contents

Form 16: TDS Certificate issued by Employer

Employers are required to deduct TDS (Tax Deducted at Source) on salary payments to employees if the total income of the employee exceeds the basic exemption limit. To provide proof of the TDS deducted and deposited on their salary income, employers issue Form 16, which is a TDS certificate, to employees every financial year.

The due date for issuing Form 16 is 15th June following the end of the financial year. Therefore, for the financial year 2021-22 (assessment year 2022-23), employers must issue Form 16 by 15th June 2022. This ensures that employees have the necessary documentation to accurately file their income tax returns.

Update Regarding Form 16 FY 2020-21 (AY 2021-22) onwards

A significant update in Form 16, concerning the new tax regime, appears in Part B of the form. The change is in Section A, where the first line now includes a question: ‘Whether opting for taxation under Section 115BAC?’ This section provides the option to select ‘Yes’ or ‘No,’ indicating whether the employee has chosen to be taxed under the new tax regime as per Section 115BAC of the Income Tax Act. This regime offers concessional tax rates but disallows certain exemptions and deductions.

What is Form 16?

Form 16 is a TDS (Tax Deducted at Source) certificate for salary, detailing the income earned and taxes deducted. It is divided into two parts: Part A and Part B. Employers can download both parts from their account on the TRACES portal.

Importance of Form 16 for Filing Income Tax Returns

Using Form 16 makes it easier to file your Income Tax Return (ITR). You can upload it on platforms like Quicko, which will automatically prepare your ITR. Besides Form 16, other important income tax documents include Form 26AS, Form 12BB, Form 10BA, and Form 15G/15H.

Form 16 Format – FY 2020-21 (AY 2021-22)

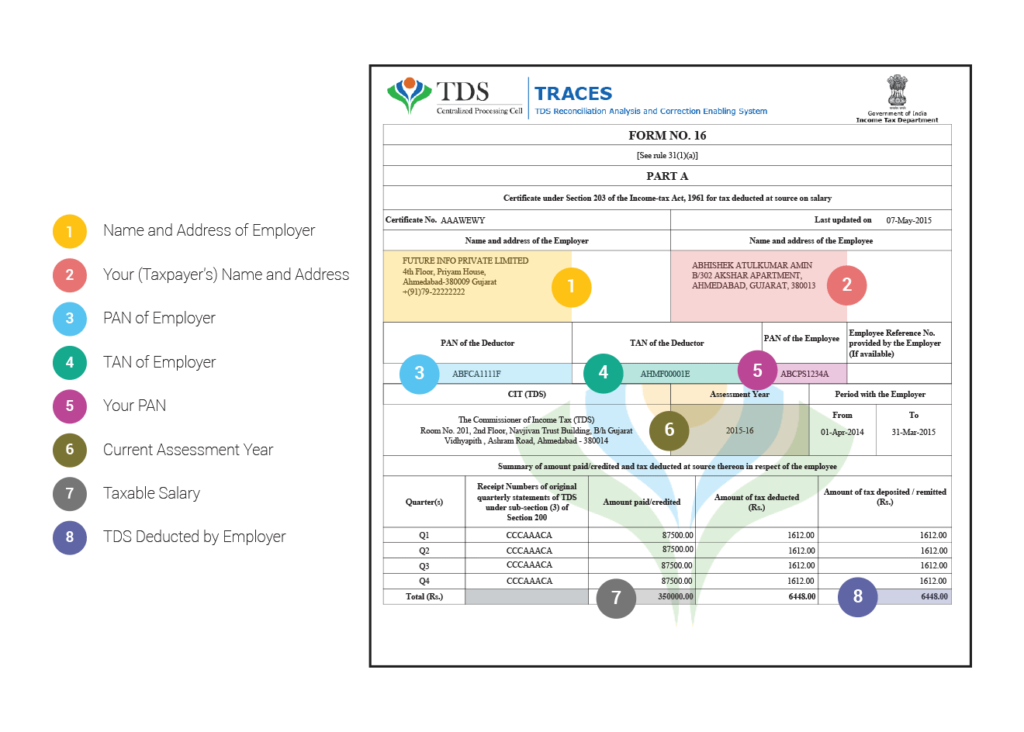

Part A of Form 16

Part A contains details of the TDS deducted by the employer. This part is generated by TRACES and includes the following information:

- Employer Details: Name, Address, PAN, TAN

- Employee Details: Name, PAN

- Tax Details: Tax deducted and deposited on the employee’s behalf

How to Use Form 16

By providing a comprehensive summary of your salary income and TDS, Form 16 simplifies the process of filing your ITR. You can cross-check the details in Form 16 with other income tax documents like Form 26AS to ensure accuracy. If you haven’t received Form 16, check your Form 26AS for TDS credits or contact your employer.

Sample Form 16 – Part A

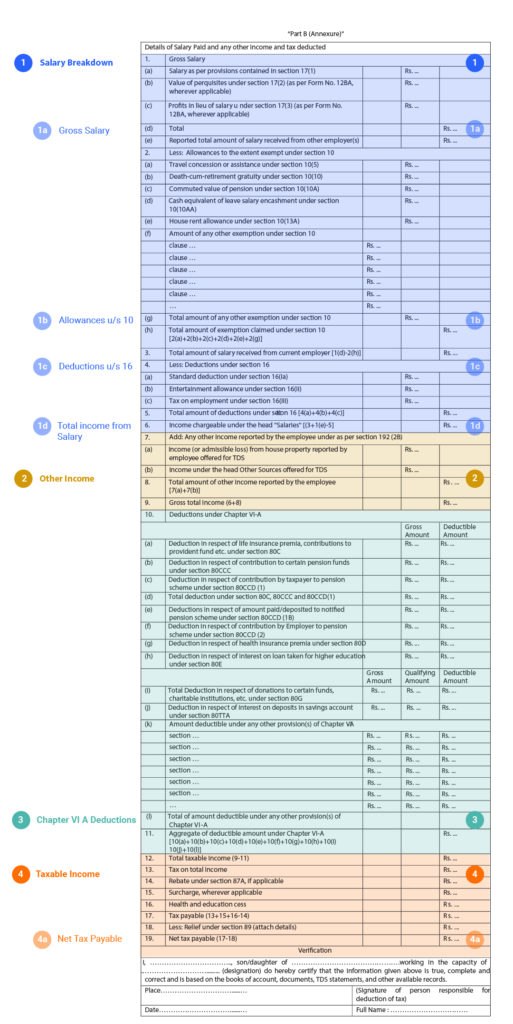

Form 16 – Part B

Part B of Form 16 is an annexure that details the Income Chargeable under the head ‘Salary’. It breaks down the salary into various components, such as allowances, perquisites, bonuses, income tax deductions, taxable income, taxes, and TDS (Tax Deducted at Source). Starting from FY 2018-19, employers are required to issue Part B of Form 16 in a standard format prescribed by the Income Tax Department.

Sample Form 16 – Part B

Salary Breakdown

Gross Salary

Gross Salary is the total remuneration received by an employee from their employer before any deductions like taxes, provident fund, etc. It includes:

- Basic Salary:

- The fixed part of the salary received every month.

- Includes gratuity, pension, advance salary, commission, etc.

- Perquisites:

- Additional benefits such as rent-free accommodation, concession in rent.

- Employer-incurred expenses on behalf of the employee like medical and educational expenses.

- Profits:

- Amount received from the current or former employer in connection with termination, such as bonuses.

- Salary from Other Employer(s):

- Salary from previous employers is included in the current gross salary when an employee switches jobs during the financial year.

Allowances under Section 10

Allowances are additional compensations provided by employers to meet specific requirements:

- Leave Travel Allowance (LTA):

- For travel within India while on leave, alone or with family.

- House Rent Allowance (HRA):

- To cover accommodation expenses for salaried individuals living in rental premises.

- Death-cum-Retirement Gratuity:

- For employees covered under the Gratuity Act, 1972. The amount is tax-exempt based on a predefined formula.

- Commuted Value of Pension:

- For government and other employees receiving a commuted pension.

- Leave Salary Encashment:

- Retirement benefit for encashing leave, tax-exempt as per a predefined formula.

Deductions under Section 16

These deductions help reduce the overall tax liability based on investments made and expenses incurred:

- Standard Deduction:

- A flat deduction from salary. No proof required. Allowed deduction is INR 50,000 for FY 2019-20.

- Entertainment Allowance:

- Exempt for government employees, up to INR 5,000.

- Employment Tax (Professional Tax):

- Paid by the employer to the state government on behalf of the employee, ranging from INR 2,400 to INR 2,500.

Calculation of Total Taxable Salary

Total taxable salary is derived after deducting the allowances under Section 10 and claiming deductions under Section 16 from the gross salary.

Other Income

- Income from Other Sources:

- Includes dividend, interest income from savings accounts, fixed deposits, etc.

- Income from House Property:

- Rental income from properties like flats, office spaces, and farmhouses.

- Includes interest and principal repayment of a loan taken on self-occupied house property.

Chapter VI-A Deductions

These deductions are from specific investments and expenses:

- 80C:

- ELSS, Provident Fund, Life Insurance Premium, etc.

- 80CCC:

- Pension Funds

- 80D:

- Medical Insurance Premium

- 80E:

- Interest on Loan taken for Higher Education

- 80G:

- Donations to Charitable Trusts, Institutions

- 80TTA or 80TTB:

- Interest on Savings and Deposits

Calculation of Total Taxable Income

Total taxable income is the sum of income from all sources after claiming exempt allowances and deductions during the financial year.

Net Tax Payable

- Net Income:

- Tax deducted on income at the applicable slab rate. Includes Income Tax, Surcharge, Health & Education Cess, Interest Penalties, etc.

- Tax Payable:

- Calculated at slab rate on net income. Includes Surcharge and Health & Education Cess. Rebates under Section 87A and relief under Section 89 are applied based on total income earned by the employee.

Raed More: Form 16A: TDS on Income other than Salary

Web Stories: Form 16A: TDS on Income other than Salary

Official Income Tax Return filing website: https://incometaxindia.gov.in/

0 Comments