Important Keyword: Due date, ITR Form, Kotak Securities, P&L Statement, Tax Audit, Trading Income.

Table of Contents

How to File ITR for Kotak Securities?

As a trader with Kotak Securities, it’s essential to navigate the complexities of filing your income tax return (ITR) correctly, especially if your earnings stem from equity trading, mutual funds, or derivatives. Kotak Securities facilitates this process by providing a Tax P&L Report summarizing your trading activities throughout the financial year. This report serves as a crucial tool in determining the appropriate ITR Form to use and assessing whether a Tax Audit is necessary.

For traders, understanding which ITR Form aligns with their income profile is key. The Tax P&L Report from Kotak Securities consolidates all trading transactions, offering clarity on gains, losses, and overall profitability. This detailed breakdown simplifies the filing process, ensuring compliance with tax regulations while maximizing potential deductions and exemptions.

Tax P&L Report Tabs Explained

When managing your taxes as a trader with Kotak Securities, it’s important to understand the nuances of filing your Income Tax Return (ITR) correctly. Kotak Securities provides detailed segment statements rather than a consolidated Tax P&L Statement. This means you’ll need to download statements for each segment separately, such as equity, derivatives, and mutual funds.

To determine the appropriate ITR Form for your filing, consider the nature of your income:

Income from Trading:

If your income primarily consists of capital gains from trading, you should file ITR-2. This form is suitable for reporting income from investments, including gains or losses from equity trading and mutual funds.

Business Income:

If your trading activities are substantial and qualify as business income (such as frequent trading in derivatives or speculative activities), you should file ITR-3. This form is designed for individuals and Hindu Undivided Families (HUFs) who have income from business or profession.

Key Components of Tax P&L Statements:

Cost Basis: The original value of assets for tax purposes, adjusted for factors like stock splits and dividends.

Proceeds: Cash received from selling assets, categorized as gross or net based on transaction details.

Square Off: A trading strategy involving the purchase and subsequent sale (or vice versa) of assets within the same trading day.

Due Date for Filing ITR:

ITR filing deadlines are specified under Section 139 of the Income Tax Act and vary based on the type of taxpayer. Generally, for individuals and HUFs not subject to audit, the due date is July 31st of the assessment year following the financial year.

Ensuring accurate and timely filing of your ITR is crucial to compliance with tax regulations. By using the segmented statements provided by Kotak Securities and understanding the distinctions between ITR-2 and ITR-3, you can effectively report your trading income and fulfill your tax obligations efficiently. Due dates for different category of taxpayers are as follows:

Category

Due Date

Individuals to whom audit is not applicable

31st July of the Assessment Year

Companies

30th September of the Assessment Year

Individuals to whom audit is applicable

30th September of the Assessment Year

Individuals/ HUF who are partners in a firm and firm’s accounts are subject to audit

30th September of the Assessment Year

The above due dates can be extended by the IT Department via order.

Tax Audit Applicability

For stock traders engaged in various types of trading activities such as Equity Intraday, Equity Futures & Options (F&O), Commodity Trading, and Currency Trading, it’s crucial to understand the tax implications, particularly whether Tax Audit under Section 44AB of the Income Tax Act applies.

Nature of Income:

Income derived from trading in shares, securities, commodities, and currencies is treated as Business Income if:

Equity Intraday: Buying and selling of stocks on the same day.

Equity Futures & Options (F&O): Contracts traded on the stock exchanges for futures and options.

Commodity Trading: Trading in commodities on recognized commodity exchanges.

Currency Trading: Trading in foreign currencies through recognized platforms.

Applicability of Tax Audit:

Tax Audit under Section 44AB becomes applicable if the turnover from these trading activities exceeds certain thresholds:

Turnover Limit under Sec 44AB:

The turnover threshold for applicability of Tax Audit is typically Rs. 1 crore.

However, Budget 2020 increased this threshold to Rs. 5 crore, provided certain conditions are met:

Cash Payments should not exceed 5% of the Total Payments in the financial year.

Cash Receipts should not exceed 5% of the Total Receipts in the financial year.

Calculation of Trading Turnover:

Definition: Trading turnover refers to the total of the amounts received or receivable from the sale of goods or services in the financial year.

Importance: It’s essential to calculate trading turnover accurately to determine whether Tax Audit is mandatory under the Income Tax Act.

Distinction between Business Income and Capital Gains:

Business Income: Income from trading activities as part of a business or profession.

Capital Gains: Income from the sale of assets such as stocks or securities held as investments.

Important Keyword: Due date, ITR Form, Motilal Oswal Trader, P&L Statement, Tax Audit, Trading Income.

Table of Contents

How to File ITR for Motilal Oswal?

For traders with Motilal Oswal, understanding how to file their Income Tax Return (ITR) is crucial, especially when income arises from trading in equity, mutual funds, or derivatives. Motilal Oswal provides a detailed Tax P&L Report summarizing all trading activities conducted throughout the financial year. This report serves as a pivotal tool, guiding traders to determine the appropriate ITR Form to file and whether a Tax Audit is necessary.

The Tax P&L Report simplifies the process by consolidating trading transactions into a comprehensive statement. This statement not only helps traders in assessing their taxable income but also aids in identifying deductions and exemptions applicable under the Income Tax Act.

Motilal Oswal: Tax P&L Statement Tabs Explained

For Motilal Oswal traders in India, the applicable Income Tax Return (ITR) form depends on the nature of income earned from trading activities:

ITR-2: This form is used if the income is from capital gains. Capital gains can arise from the sale of securities such as stocks, mutual funds, etc. Therefore, if you are trading and earning income primarily through capital gains (short-term or long-term), you would file ITR-2.

ITR-3: This form is applicable if the income is from business or profession. If your trading activities are substantial, frequent, and qualify as a business activity rather than just occasional investments, you would file ITR-3. Business income includes profits or losses from trading activities where there is regular buying and selling of securities with the intent to earn profit.

Key Points Motilal Oswal:

Capital Gains (ITR-2): If you primarily earn income from the sale of securities and it qualifies as capital gains (whether short-term or long-term), use ITR-2.

Business Income (ITR-3): If your trading activities are extensive, frequent, and you consider it as a business where you actively buy and sell securities, use ITR-3.

Due Date for Filing ITR:

The due date for filing Income Tax Returns for individuals, including traders, is typically:

31st July of the assessment year for non-audit cases (where audit is not required under any law).

Due dates for different category of taxpayers are as follows:

Category

Due Date

Individuals to whom audit is not applicable

31st July of the Assessment Year

Companies

30th September of the Assessment Year

Individuals to whom audit is applicable

30th September of the Assessment Year

Individuals/ HUF who are partners in a firm and firm’s accounts are subject to audit

30th September of the Assessment Year

The above due dates can be extended by the IT Department via order.

Tax Audit Applicability

To determine whether a tax audit is applicable under Section 44AB of the Income Tax Act for traders engaged in activities like Equity Intraday, Equity F&O, Commodity Trading, and Currency Trading, you need to calculate the trading turnover. Here’s how you can approach it:

Calculation of Trading Turnover:

Equity Intraday, Equity F&O, Commodity Trading, and Currency Trading are considered as Business Income:

Income from these activities is treated as business income, not capital gains.

Definition of Turnover:

Equity Intraday: Total of positive and negative differences resulting from transactions in the financial year.

Equity F&O: Absolute value of sum of both positive and negative differences on settlement of contracts.

Commodity Trading: Absolute value of sum of both positive and negative differences on settlement of contracts.

Currency Trading: Absolute value of sum of both positive and negative differences on settlement of contracts.

Conditions for Tax Audit Applicability (Budget 2020 Amendment):

The turnover threshold for applicability of tax audit under Section 44AB has been increased from Rs. 1 crore to Rs. 5 crores, provided:

Cash payments do not exceed 5% of the total payments in the financial year.

Cash receipts do not exceed 5% of the total receipts in the financial year.

Calculation of Turnover:

Calculate the total of positive and negative differences from all trading activities (Equity Intraday, Equity F&O, Commodity Trading, Currency Trading) over the financial year.

This turnover figure is crucial for determining whether the trader exceeds the threshold requiring a tax audit.

Example Scenario:

Suppose a trader has the following turnover figures for the financial year from Equity Intraday, Equity F&O, Commodity Trading, and Currency Trading:

Equity Intraday: Rs. 3,00,00,000 (absolute value of differences)

Equity F&O: Rs. 1,50,00,000 (absolute value of differences)

Commodity Trading: Rs. 80,00,000 (absolute value of differences)

Currency Trading: Rs. 2,00,00,000 (absolute value of differences)

Since the total turnover exceeds Rs. 5 crores, a tax audit would be mandatory for this trader unless the conditions related to cash transactions (not exceeding 5% of total payments and receipts) are satisfied.

Important Keyword: Due date, ITR Form, P&L Statement, Tax Audit, Trading Income, Upstox Traders.

Table of Contents

How to File ITR for Upstox?

As a trader using Upstox, your journey in filing your Income Tax Return (ITR) revolves around the comprehensive Tax P&L Report provided by the platform. This report amalgamates all your trading activities across equities, mutual funds, and derivatives throughout the financial year. Understanding this document is crucial as it determines which ITR form you should file and whether a Tax Audit is applicable.

The Tax P&L Report serves as your compass in navigating the complexities of tax compliance. It outlines your gains and losses from trading, essential for accurate reporting to the Income Tax Department. Based on the report’s insights, you can ascertain the appropriate ITR form that aligns with your trading income profile.

For those new to the process, filing taxes can seem daunting, but with Upstox’s intuitive tools and guidance, the journey becomes more accessible. By leveraging the Tax P&L Report, you gain clarity on your financial obligations, ensuring compliance while maximizing your returns.

Upstox Tax P&L Statement Tabs Explained

For Upstox traders, the applicable Income Tax Return (ITR) form depends on the nature of income earned from trading activities:

ITR-2: This form is used when the income from trading includes capital gains income. Capital gains can be either short-term or long-term depending on the holding period of the assets traded.

ITR-3: This form is used when the income from trading includes business income. Business income typically arises when the trading activity is frequent and substantial, resembling a business operation rather than mere investment.

Key Points Upstox:

If your trading activities result in income categorized as capital gains (whether short-term or long-term), you should file ITR-2.

If your trading activities qualify as business income (due to frequency, volume, and intention to earn profit), you should file ITR-3.

Due Date for Filing ITR: The due dates for filing Income Tax Returns are specified under Section 139 of the Income Tax Act and are typically:

31st July of the assessment year for individuals (unless extended by the tax authorities).

It’s important to file your ITR within the due date to avoid penalties and interest on late filing, if applicable.

Due dates for different category of taxpayers are as follows:

Category

Due Date

Individuals to whom audit is not applicable

31st July of the Assessment Year

Companies

30th September of the Assessment Year

Individuals to whom audit is applicable

30th September of the Assessment Year

Individuals/ HUF who are partners in a firm and firm’s accounts are subject to audit

30th September of the Assessment Year

The above due dates can be extended by the IT Department via order.

Tax Audit Applicability

When determining the applicability of Tax Audit under Section 44AB of the Income Tax Act for income derived from trading in shares, securities, commodities, and currencies as business income, it’s crucial to calculate the trading turnover accurately. Here’s how you can approach it:

Definition of Trading Turnover

Trading turnover is computed based on the total of the following:

Total of Positive and Negative Differences:

In case of trading in derivatives (like Equity F&O, Commodity Futures, Currency Futures), turnover includes both positive and negative differences.

Speculative Transactions:

For equity intraday trading (where delivery does not happen), the total of both buying and selling transactions is considered as turnover.

Gross Total Income:

The aggregate of income under all heads like salary, house property, business or profession, capital gains, and income from other sources.

Conditions for Tax Audit Applicability (Budget 2020 Amendment)

According to the Budget 2020 amendment, the turnover limit under Section 44AB has been increased from Rs. 1 crore to Rs. 5 crore for traders in shares, securities, commodities, and currencies, provided the following conditions are met in the financial year:

Cash Payments: Cash payments do not exceed 5% of the total payments.

Cash Receipts: Cash receipts do not exceed 5% of the total receipts.

Steps to Calculate Trading Turnover

Equity Intraday Trading:

Sum up the total of all buying and selling transactions (including turnover of shares where intraday trading has occurred).

Equity Futures & Options (F&O):

Include the absolute value of both positive and negative differences i.e., the sum total of all profits and losses.

Commodity Trading:

Compute the total of all transactions (buying and selling) including both profit and loss.

Currency Trading:

Similarly, aggregate all transactions (buying and selling) across the currency pairs traded.

Example Calculation:

If you’re trading in equity futures and options:

Total of all positive and negative differences (absolute value) across all contracts traded during the financial year.

For equity intraday:

Total of all buy and sell transactions where shares were traded on the same day.

Important Keyword: Due date, ITR Form, P&L Statement, Sharekhan, Tax Audit, Trading Income.

Table of Contents

How to File ITR Formfor Sharekhan?

For a trader using Sharekhan, filing an Income Tax Return (ITR) hinges on the income derived from trading in equity, mutual funds, or derivatives. Sharekhan facilitates this process by providing a Tax P&L Report that consolidates all trading transactions conducted throughout the financial year. This report serves two primary purposes:

ITR Form Determination: The trader can ascertain which ITR form to file based on the types of trading income reported in the Tax P&L Report. Generally, income from equity, mutual funds, and derivatives is considered business income.

Tax Audit Applicability: Using the Tax P&L Report, traders can also evaluate whether their trading turnover meets the thresholds that require a Tax Audit under the provisions of the Income Tax Act.

Tax P&L Statement of Sharekhan Explained

Sharekhan provides statements from the portal, but these are not consolidated. Therefore, traders need to download separate statements for different segments. Here’s a breakdown of the tabs mentioned in these statements:

Holding Period: This refers to the duration for which an asset or portfolio was held. It is a key measure of investment performance.

Realized Gain/Loss: It indicates the profit or loss realized upon completing a trade.

Short Term Transactions: These involve trading strategies where assets are bought and sold within a relatively short period, typically ranging from days to weeks.

Long Term Transactions: These involve capital assets held for more than one year, which are generally categorized as long-term investments.

Speculation Transactions: These involve transactions where contracts for purchase or sale of commodities or securities are settled without physical delivery or transfer.

Applicable ITR Form for Sharekhan Traders:

Nature of Income: Income from trading in equity, mutual funds, or derivatives through Sharekhan is typically classified as business income.

ITR Form: Based on the nature of trading income:

Capital Gains Income: File ITR-2.

Business Income: File ITR-3.

Due Date for Filing ITR:

Income Tax Return (ITR) filing for Sharekhan traders follows the due dates specified under Section 139 of the Income Tax Act. These dates vary based on the type of taxpayer and the specifics of their income situation. It is essential for traders to adhere to these deadlines to avoid penalties and ensure compliance with tax regulations.

Therefore, due dates for different category of taxpayers are as follows:

Category

Due Date

Individuals to whom audit is not applicable

31st July of the Assessment Year

Companies

30th September of the Assessment Year

Individuals to whom audit is applicable

30th September of the Assessment Year

Individuals/ HUF who are partners in a firm and firm’s accounts are subject to audit

30th September of the Assessment Year

To add, the above due dates can be extended by the IT Department via order.

Tax Audit Applicability for Sharekhan

For Sharekhan traders involved in trading shares, securities, commodities, and currencies, including activities like Equity Intraday, Equity Futures & Options (F&O), Commodity Trading, and Currency Trading, income generated is classified as Business Income. It’s crucial to assess whether a Tax Audit is applicable under the provisions of the Income Tax Act.

Applicability of Tax Audit:

Under Section 44AB of the Income Tax Act:

The turnover limit for requiring a Tax Audit is Rs. 1 crore.

However, Budget 2020 increased this turnover limit to Rs. 5 crore under specific conditions:

Cash Payments do not exceed 5% of the Total Payments in the financial year.

Cash Receipts do not exceed 5% of the Total Receipts in the financial year.

Calculation of Trading Turnover for Sharekhan:

Nature of Income: Income from trading in shares and securities through Sharekhan is treated as business income.

Tax Audit Determination: The turnover for the purpose of Tax Audit is calculated as the aggregate value of all trading transactions conducted during the financial year. This calculation is relevant only when the trading income is classified as business income and not capital gains income.

Tax Liability: It’s important to note that while the requirement for a Tax Audit depends on turnover, the actual tax liability is determined based on the total taxable income, which includes business income and other sources.

Important Keyword: Due date, IT Notice, Section 139(5), Section 143(1)(a).

Table of Contents

Section 143(1)(a): Notice for Proposed Adjustments

The Income Tax Department verifies the details provided in the return filed by the taxpayer. If there are any discrepancies, the department issues a notice or intimation to the taxpayer, instructing them to make corrections. Before starting any assessment procedure, the department issues a notice under Section 143(1)(a), which outlines the proposed adjustments to the return. After the taxpayer responds to this notice, the department begins the assessment procedures and issues a final order.

What is Notice Under Section 143(1)(a)

Section 143(1)(a) notice of proposed adjustments involves the electronic processing of tax returns by the Centralized Processing Center (CPC) in Bengaluru. This notice is a preliminary communication and not a final assessment. It indicates discrepancies or adjustments in the filed income tax return based on the provided information. The taxpayer is given the opportunity to respond to these proposed adjustments before a final assessment is made.

Such notice is issued for the following reasons:

Section

Reason

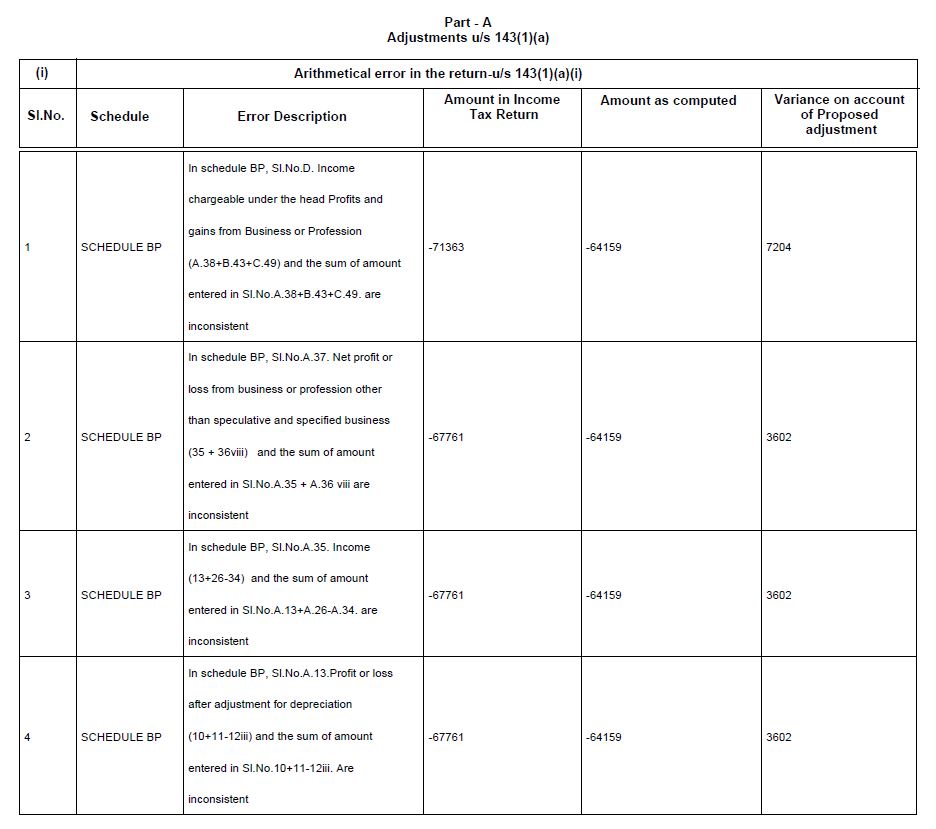

143(1)(a)(i)

Arithmetical Error in ITR

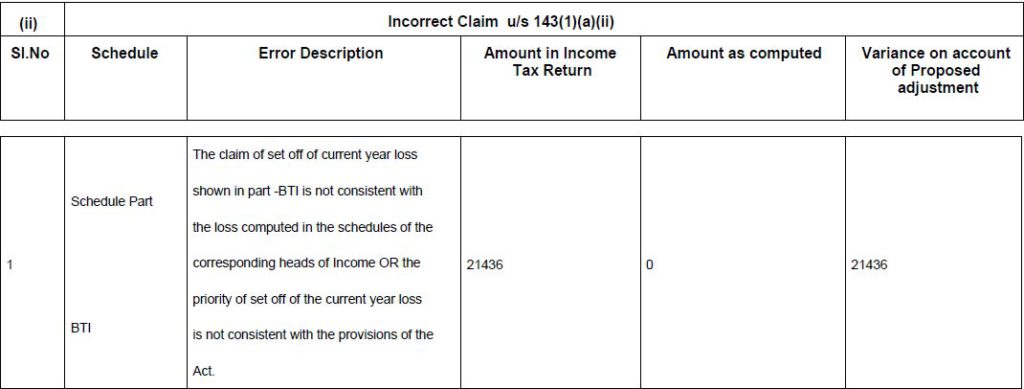

143(1)(a)(ii)

Incorrect Claim in ITR

143(1)(a)(iii)

Disallowance of loss claimed in ITR

143(1)(a)(iv)

Disallowance of expense claimed in ITR

143(1)(a)(v)

Disallowance of deduction claimed in ITR

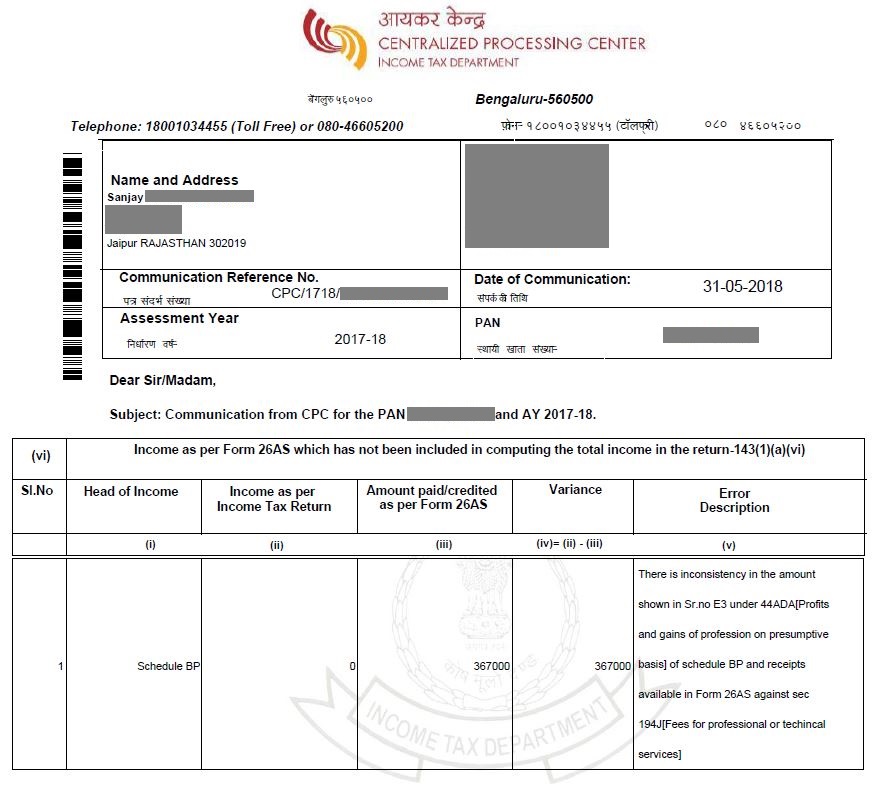

143(1)(a)(vi)

Addition of income appearing in Form 26AS, Form 16 or Form 16A

Notice u/s 143(1)(a)(i)

Notice under this sub-section is issued when there is an arithmetical error in the return. The notice specifies the income categories where discrepancies exist between the calculations based on the taxpayer’s filed return and the department’s calculations.

Notice u/s 143(1)(a)(ii)

A notice under this sub-section is sent when there are discrepancies in the Income Tax Return you have filed. An incorrect claim in your return can occur in the following situations:

Mismatch of Information: The details provided in one section of your Income Tax Return do not align with the information given in another section.

Omission of Required Information: Important details that should be included in the return are missing.

Exceeding Deduction Limits: The deductions claimed in the return go beyond the allowable limits set by the Income Tax Act.

Notice u/s 143(1)(a)(iii)

If you file your Income Tax Return after the due date specified under section 139(1), you are not allowed to carry forward losses. If you still claim these losses, the Income Tax Department will issue a notice under section 143(1)(a)(iii) to disallow them.

Notice u/s 143(1)(a)(iv)

This notice is sent when an expense has been incorrectly claimed in the Income Tax Return. If the audit report disallows certain expenses and you claim them while filing your return, these will be disallowed, and you will receive a notice under section 143(1)(a)(iv).

Notice u/s 143(1)(a)(v)

A notice under this sub-section is issued if you have incorrectly claimed certain deductions in your Income Tax Return. Deductions under sections like Sec 10AA and Sec 80H to Sec 80RRB in Chapter VI-A cannot be claimed if the return is filed after the due date specified under section 139(4). If these deductions are claimed, a notice under section 143(1)(a)(v) will be issued to disallow them.

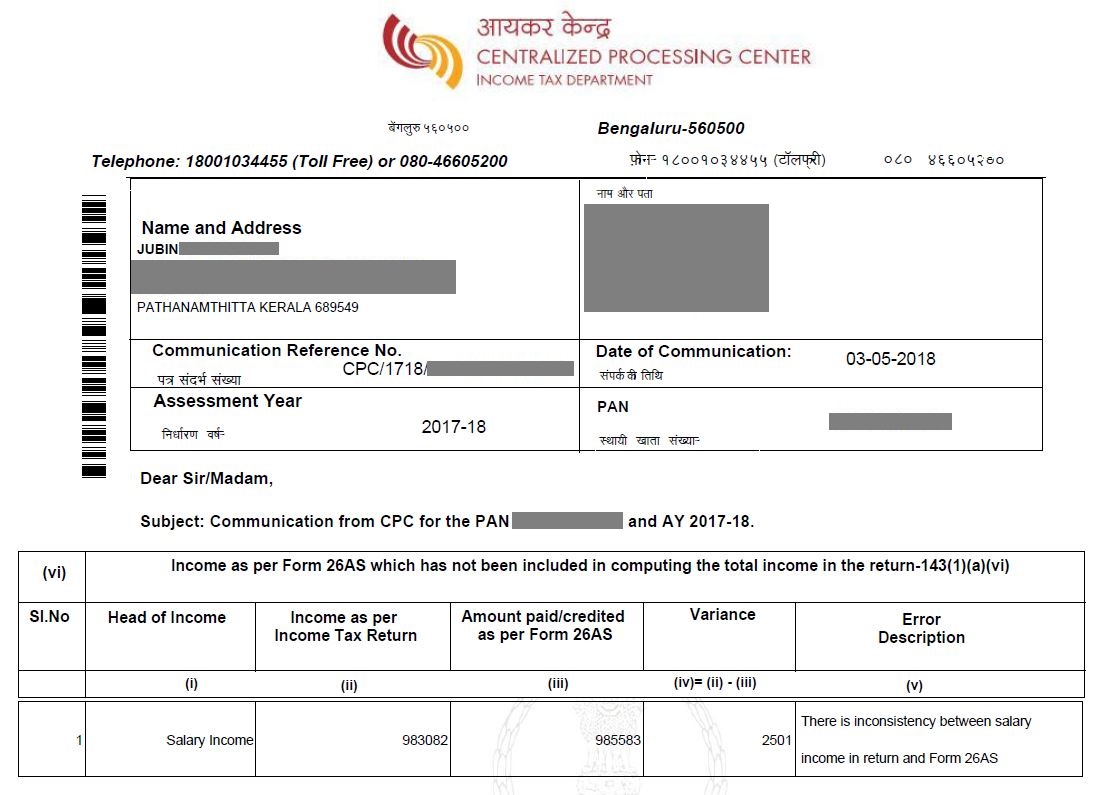

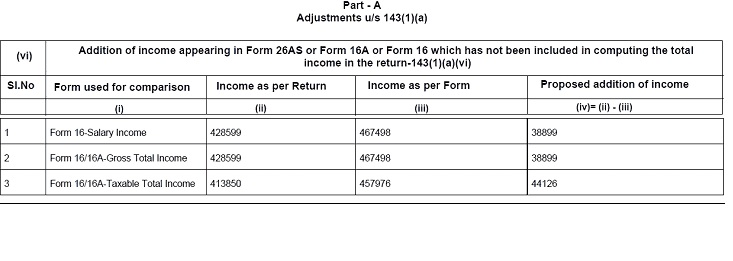

Notice u/s 143(1)(a)(vi)

This notice is received when there is a mismatch between the details of TDS (Tax Deducted at Source) on salary as per Form 26AS or Form 16 and the TDS details reported in the Income Tax Return. There can also be mismatches between TDS as per Form 16A and the income details reported. Specifically, this can occur if the Business or Profession Income reported under Schedule BP in the return does not match the gross receipts or turnover in the Tax Credit Statement (Form 26AS).

The salary reported under Schedule S in the return does not match the gross salary in the Tax Credit Statement i.e. Form 26AS.

Taxable Salary in ITR does not match with the Taxable Salary as per Form 16. This indicates that the taxpayer has included an additional deduction in the ITR that doesn’t appear in Form 16.

Communication of proposed adjustment u/s 143(1)(a)

Notification Process by the CPC The Central Processing Centre (CPC) at the income tax portal will send the intimation letter under section 143(1)(a) to your registered email or mobile number. This notice will be password-protected. To open it, use your PAN in lowercase followed by your date of birth in DDMMYYYY format. For example, if your PAN is AAGPR1212A and your date of birth is 02/10/1980, the password will be aagpr1212a02101980.

Time Limit for Issuing the Notice The Income Tax Department can issue this notice within nine months from the end of the financial year in which the return is filed. For example, if Ms. Priya filed her income tax return on 25th July 2023, she could receive a notice under section 143(1)(a) until 31st December 2024. This period allows for 9 months from the end of the financial year in which the return was filed.

If you do not receive any intimation within this period, it means that the calculations of the Income Tax Department matched the details provided in your filed return.

Due Date for Submitting a Response Upon receiving a notice under section 143(1)(a), you must file a response within 30 days from the date of the notice. Your options include:

Agreeing to the Discrepancies

Accept the proposed adjustments.

Disagreeing with the Discrepancies

Submit a response explaining your reasons for disagreement.

Partially Agreeing to the Discrepancies

Submit a response explaining which parts you disagree with and why.

In any of the above cases, you have the option to submit a revised return under section 139(5).

How to File Response to Notice u/s 143(1)(a)

Login to the e-filing portal and navigate to Pending Actions > e-Proceedings from the dashboard.

View NoticesClick on the option to View Notice for adjustment u/s 143(1)

Notice pdfClick on the Notice/Letter pdf.

Download the noticeYou will be able to view the notice issued to you. If you wish to download the notice, click Download.

Respond to NoticeClick on the option to submit a response.

Details of the Prima Facie AdjustmentsYou will be able to view the details of the Prima Facie Adjustments found by CPC in your filed ITR. Click on each variance to respond.

Provide ResponseOn clicking the variance, details of the variance will be there. To respond to the particular variance, click Provide Response.

Response from dropdownSelect the relevant response from the dropdown and click Save after responding to each Prima Facie Adjustment.

Proceed to e-verify your responseAfter providing all the responses, click “Back.” This action will take you to the details of the Prima Facie Adjustment that CPC found in your filed ITR. Once you respond to each variance, the system will save your responses. Click Continue, Select the Declaration checkbox, and click Proceed to e-Verify.

Successful VerificationOn successful e-Verification, a success message will be there along with a Transaction ID. You will also receive a confirmation message on your email ID registered on the e-filing.