Important Keyword: Form 26AS, Income Heads, TDS Certificate.

Table of Contents

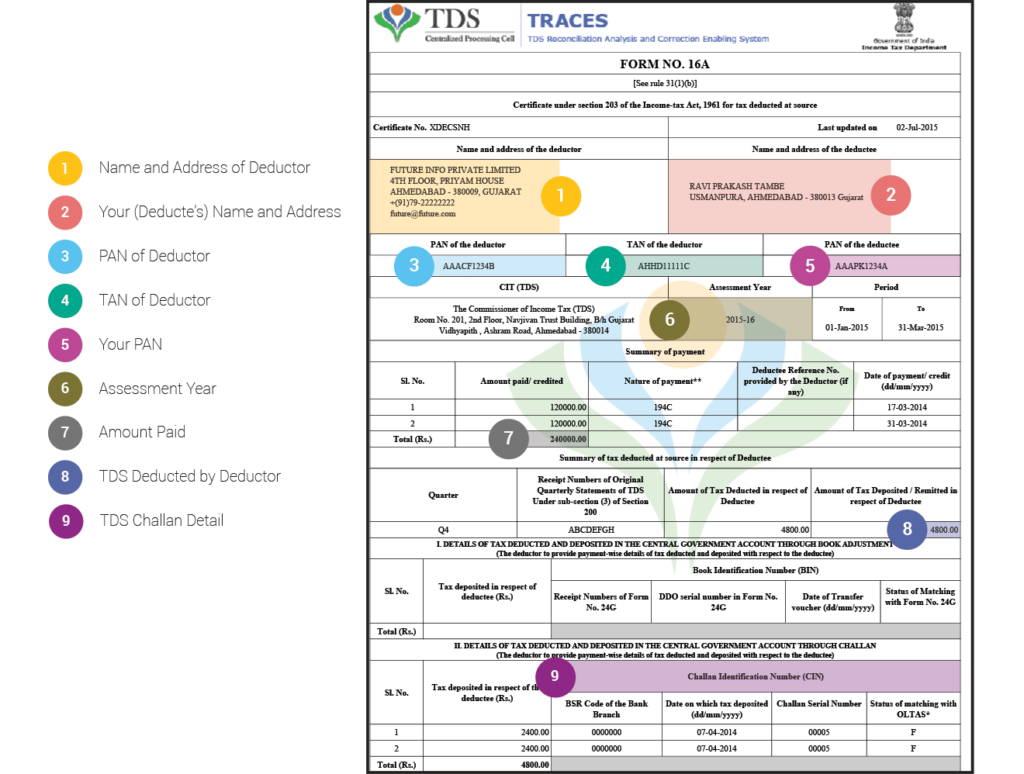

What is Form 16A?

Form 16A serves as a certificate of TDS (Tax Deducted at Source) specifically on income other than salary. This includes payments such as commission, contract fees, professional charges, rent, interest, etc.

Issued by the deductor to the deductee, the deductor, also known as the payer, is the individual or entity making the payment and deducting TDS. The deductee, or payee, is the recipient of the payment from whom TDS is deducted.

The deductor holds the responsibility of issuing Form 16A to the deductee within 15 days from the date of filing the TDS Return. This ensures that the deductee has documentation verifying the TDS deduction on their income other than salary.

It distinguishes itself from Form 16 by being specifically designated for TDS (Tax Deducted at Source) on income apart from salary, unlike Form 16 which pertains to TDS on salary.

Here are the essential details:

Deductor Information:

Name, address, PAN (Permanent Account Number), and TAN (Tax Deduction and Collection Account Number) of the Deductor.

Deductee Information:

Name, address, and PAN of the Deductee (the individual or entity from whom TDS is deducted).

Payment Details:

Nature of the Payment: Description of the income for which TDS is deducted (e.g., commission, professional fees, rent, interest, etc.).

Amount Paid: The total amount paid to the deductee.

Date of Payment: The date on which the payment was made to the deductee.

TDS Challan Details:

Details of the TDS challan, including the challan number, date of deposit, and amount of TDS deposited with the government.

It provides a comprehensive overview of the TDS deducted on income sources other than salary, ensuring transparency and compliance with tax regulations for both the deductor and the deductee.

The provision of Form 16A to the deductee as proof of tax deduction falls under the responsibility of the deductor. In case the deductee has not received Form 16A, they can verify the TDS credit by referring to their Form 26AS.

The deductor can access and download Form 16A from their account on TRACES (TDS Reconciliation Analysis and Correction Enabling System). This platform facilitates the management and issuance of various TDS-related documents, ensuring transparency and compliance with tax regulations.

Important Keyword: Income Heads, Income Tax, ITR Forms & Documents, Section 80GG.

Table of Contents

What is Form 10BA?

Form 10BA serves as a declaration for taxpayers seeking a deduction under section 80GG for rent paid on rental property. To claim this deduction, two conditions must be met: the taxpayer must be self-employed or salaried without receiving HRA from an employer, and the taxpayer, their spouse, minor child, or HUF (if applicable) should not own any self-occupied residential accommodation.

To file Form, taxpayers need to provide their name, PAN, address of the rental property, rental details, and the name and address of the landlord.

Let’s illustrate with an example: Arun worked as an employee for the first six months of FY 2019-20 and then transitioned to freelancing. Throughout the year, he resided in rented premises. While employed, he received HRA and does not own any self-occupied property. In this scenario, Arun is eligible to claim a deduction under section 80GG by filing Form 10BA for the rent paid during the last six months, as he did not receive HRA during that period and did not own any self-occupied property.

When to file Form 10BA?

it’s essential to file Form 10BA before submitting the Income Tax Return (ITR) if you intend to claim a deduction under section 80GG for the rent paid. This form serves as a declaration to support your claim for the deduction. Therefore, it’s necessary to complete this step before filing your ITR to ensure that your claim for the deduction is valid and compliant with tax regulations.

How to file Form 10BA online?

A taxpayer has to submit the form online on the e-filing portal. Following are the steps to file.

Go to the Income Tax e-Filing Portal and login to your account by entering your User ID/ PAN/ TAN and password

On the dashboard navigate to e-file > Income Tax Forms> File Income Tax Forms

Search for Form 10BA under the category “Person not dependent on any Source of Income” and click on “File Now”

Select the relevant assessment year and click “Continue” and on the next screen click on “Let’s Get Started”

Provide details for each selection> Click on House Property Details> Enter the required details like the Address of the rented property, Name and address of the Landlord, Details of Rent Paid etc. and click Save

Now click on Declaration> select the check box> click Save Preview and proceed to e-verify> select mode of e-verification and Submit> Form 10BA will be filed and e-verified successfully.

Important Keyword: Income Heads, Income Source, NRI Taxpayers, Resident Status.

Table of Contents

Definition of NRI

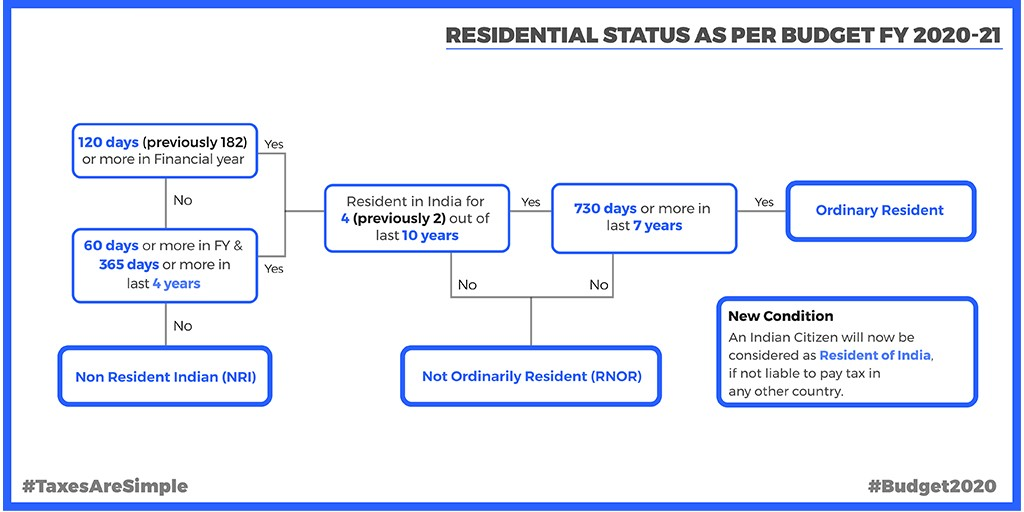

Determining the tax liability of an NRI hinges upon their residential status for the year. It’s crucial to ascertain the residential status of an individual before delving into their tax obligations. Here are the criteria for determining residential status:

You’re considered an Indian resident for a particular financial year if:

You’ve spent at least 182 days (6 months) in India during the financial year, or

You’ve resided in India for at least 60 days (2 months) during the previous year and have lived for at least 365 days (a year) during the last four years.

However, the first condition alone applies if you’re an Indian citizen working abroad or a member of a crew working on an Indian ship. In such cases, if you spend at least 182 days in India during the financial year, you’re deemed a resident Indian.

A person is considered to be of Indian origin if they, or either of their parents or any of their grandparents, were born in undivided India.

If you don’t meet any of the above conditions, then you’re categorized as an NRI.

Determining the residential status plays a pivotal role in assessing the taxability of income.

If your status for the previous year is “Resident,” your global income will be taxable in India. However, if your status is “NRI,” only the income earned or accrued in India will be taxable in India. Some examples of incomes earned or accrued in India include salary received in India, professional fees received in India, rental income from property in India, capital gains from the transfer of assets situated in India, and interest income on fixed deposits or savings accounts in India.

All these incomes are taxable in India for an NRI. Any income earned by an NRI outside India, such as salary income abroad or interest earned on NRE accounts or deposits abroad, will not be taxable in India.

It’s important to note that interest income on the NRE account is completely tax-free, while interest earned on the NRO account is subject to TDS at the rate of 30.9%.

Taxable Incomes for NRI Include

Salary earned or received in India by an NRI, or on their behalf, is taxable in India. This includes income deposited to an Indian bank account. For instance, if an Indian company employee, like Ravish, is deputed to work in Dubai but continues to receive their salary in India, that income is taxable in India.

However, salaries received by diplomats and ambassadors are completely exempt from taxation.

Income from house property situated in India is taxable for NRIs. The calculation follows the same rules as for resident Indians, including deductions like the standard 30% deduction and deductions for interest and principal repayment on home loans. Rental income received by NRIs is subject to a 30.9% TDS by the tenant.

Income from businesses set up or controlled from India is taxable for NRIs, as is income from other sources like interest on deposits or savings bank accounts in India. Interest earned on NRE and FCNR accounts is tax-exempt for NRIs, while interest earned on NRO accounts is subject to a 30.9% TDS.

Capital gains from the transfer of assets situated in India, including shares and securities, are taxable in India for NRIs. However, exemptions under sections 54 and 54EC are available for capital gains arising from the sale of residential property.

Deductions and Exemptions for NRI

Here is a summary of deductions and exemptions which are / not allowable for NRI:

Deductions/ Exemptions

Allowable

Not allowable

Section 80C

Life Insurance Premium Payment

Investment in PPF

Children’s Tuition Fee Payment

Investment in NSCs

Principal Repayment on Loan for purchase of House Property

Post Office 5 year Deposit Scheme

Investment in ELSS

Senior Citizen Saving Scheme

Investment in Unit Link Insurance Plan

Section 80CCG

–

Investment under RGESS

Section 80D

Premium Paid for Health Insurance

–

Section 80DD

–

Expenditure on Maintenance including medical treatment of a handicap dependent

Section 80DDB

–

Expenditure towards medical treatment of a differently abled dependent

80E

Interest paid on education loan

–

80G

Donations for charity (social) causes

–

80TTA

Interest income from savings bank account

–

80U

–

Deduction available to differently abled individuals

80U

–

Deduction available to differently abled individuals

Deductions from House Property Income

Standard deduction

–

Property taxes paid

Interest paid on home loan

Exemption on sale of Long term property

Section 54: On sale of long term house property

–

Section 54F: On sale of any long term asset other than house property

Section 54EC: On sale of any property and reinvestment in bonds of National Highway Authority of India (NHAI) and Rural Electrification Corporation (REC)

How to Avoid Double Taxation?

To avoid double taxation, NRIs can benefit from the Double Taxation Avoidance Agreement (DTAA), an agreement between India and foreign countries. The DTAA provides relief in two ways:

Exemption from double taxation: If the agreement allows exemption, the NRI is taxed in only one country, and no taxes are payable in the other. For instance, if Manali, a non-resident Indian, earns interest income from fixed deposits in India while working as a Certified Accountant in the US, and India and the USA have an agreement providing exemption, her interest income is taxed only in India, exempt from US taxation.

Tax Credit (Relief): If the agreement provides relief, incomes are taxed in both countries, but the NRI can claim relief in their country of residence. For example, if Paritosh, an NRI content writer in Australia, earns rental income from his flat in India, and India and Australia have an agreement providing relief via tax credit, his rental income is taxed in both countries. However, Paritosh can claim a tax credit in Australia for the taxes paid in India.

Changes in Budget 2020: The budget introduced changes affecting NRIs:

Criteria for Determining Residential Status: The condition of 182 days to determine residential status was reduced to 120 days in a financial year. An Indian national is now deemed a resident if they stay in India for at least 120 days.

Resident – Not Ordinary Resident (RNOR): The requirement for being deemed an RNOR was increased from 2 out of the previous 10 years to 4 out of the previous 10 years.

Section VI (IA) – New Clause

The Finance Minister’s latest announcement introduces a new clause, stating that if an individual isn’t a resident of any other country, they’ll be deemed a resident of India by default. Once deemed a resident, they must disclose all assets and finances, whether from India or abroad.

Dividend Distribution Tax (DDT)

Under the current tax regime, companies deduct DDT on dividends paid to shareholders. However, the new regime exempts dividends from taxation at the shareholder level. Instead, companies will deduct TDS on distributed dividends. For NRI shareholders, TDS will be deducted under section 195, and dividend income will be taxed according to slab rates.

Source of Income

Resident

Not Ordinary Resident

None-Residents

Income earned in India

Taxable in India

Taxable in India

Taxable in India

Any income received in India

Taxable in India

Taxable in India

Taxable in India

Income earned outside India but received in India

Taxable in India

Taxable in India

Taxable in India

Income earned and received outside India

Taxable in India

Taxable in India

Not Taxable in India

Any income earned outside India for a business or profession controlled in or from India

Taxable in India

Taxable in India

Not Taxable in India

Income earned outside India from any source other than business or profession controlled from India

Important Keyword: DTAA, Income Heads, Income Tax, NRI Taxpayers.

Table of Contents

DTAA – Double Taxation Avoidance Agreement: Definition, Types, and Benefits

For Non-Resident Indians (NRIs) employed in foreign countries, the Double Taxation Avoidance Agreement (DTAA) serves as a vital tool to prevent the occurrence of double taxation on income earned both in their country of residence and in India. With 85 active agreements in place, India endeavors to ensure that taxpayers in these countries are not burdened with the obligation of paying taxes twice on the same income. The primary objective of DTAA is to stimulate and facilitate economic trade and investment between two nations by circumventing instances of double taxation. To access the DTAA agreements entered into by India with various countries, individuals can refer to the income tax department’s website via the following link: Notification of Government.

What is DTAA?

DTAA, or Double Taxation Avoidance Agreement, stands as a pact between two or more nations aimed at preventing the imposition of taxes on the same income twice. This agreement comes into play when an individual resides in one country but earns income in another. Essentially, DTAA outlines the tax rates and jurisdictions applicable to income derived from each country involved.

Consider the case of Mr. Arjun, an Indian national residing in the UK. Despite his investments in India generating returns, he may face the prospect of being taxed on this income in both India and the UK. However, thanks to DTAA, Mr. Arjun is spared from double taxation. This agreement ensures that he will not be subjected to taxation for the same income in both countries, thereby offering him relief from potentially burdensome tax liabilities.

Types of DTAA

Relief from Double Taxation can be granted through bilateral treaties or unilateral relief methods. Bilateral Treaties involve agreements between two countries, where relief is determined based on mutual consent:

Exemption method: Under this approach, income is taxed in only one country, typically the country of residence.

Tax credit: Income is taxed in both countries, but relief is granted in the country where the taxpayer is a resident, usually through tax credits.

Alternatively, Unilateral Relief is provided by the taxpayer’s home country when there’s no mutual agreement between nations.

DTAA can be Comprehensive, covering various types of income, or Limited, focusing on specific types of incomes.

Advantages of DTAA include making a country more appealing for investment by offering relief on dual taxation, reducing tax evasion possibilities, and providing concessions on tax rates, including lower withholding tax.

Implementation of DTAA can occur either by exempting income earned abroad entirely or by providing a credit for tax paid in the other country.

In Mr. Arjun’s case, if the DTAA states that the UK exempts his income earned from investments in India, he will only pay taxes in India. However, if both India and the UK tax the income, Mr. Arjun will receive a tax credit for taxes paid in the UK, reducing his tax liability in India.

Nations sign DTAA to provide relief to taxpayers and stimulate investments.

To claim DTAA benefits, NRIs in DTAA countries must submit the following documents annually within the specified deadlines:

Tax Residency Certificate (TRC): Obtain TRC from tax/government authorities of the current residence country, certified through Form 10F.

Form 10F: Submit Form 10F to avail DTAA benefits.

PAN Number: Provide PAN along with other documents to claim tax benefits.

How to apply for DTAA?

Applying DTAA entails a structured approach, incorporating various provisions:

Scope Evaluation: Initially, ascertain if the matter falls within the treaty’s scope.

Tax Applicability Verification: Confirm if the tax under consideration aligns with those outlined in Article 2 or bears substantial similarity to them.

Treaty Validity Check: Ensure that the treaty is effective for the relevant taxable period.

These sequential steps help in determining the eligibility and applicability of DTAA provisions, ensuring a systematic approach to tax relief.

How is Double Taxation Avoidance Agreement relief calculated?

When DTAA is applicable, taxpayers can claim relief under section 90. Here’s how to compute Double Taxation relief:

Calculate Global Income: Sum up Indian and Foreign incomes.

Determine Tax on Global Income: Apply slab rates to compute tax.

Average Tax Rate: Find the average tax rate (Global income divided by tax amount).

Tax on Foreign Income: Multiply Foreign income by the average tax rate.

Foreign Tax Paid: Determine tax paid in the Foreign country.

Relief Calculation: Choose the lower amount between Foreign tax paid and Tax on Foreign income.

In the absence of DTAA, relief can be claimed under section 91. Here’s how:

Calculate Indian Tax: Compute tax payable in India.

Compare Tax Rates: Determine the lower tax rate between India and the Foreign country.

Tax Adjustment: Multiply the lower tax rate by the doubly taxed income.

Relief: The relief amount is as computed in the previous step.

India has signed DTAA with numerous countries, including major ones where Indians reside. Some notable countries on this list include: [List of countries].

Important Keyword: Agriculture Income, Income Heads, Income Tax.

Table of Contents

Tax on Agricultural Income

In the Union Budget of 2023-24, the government earmarked around 1.25 lakh crore rupees for agriculture and its welfare schemes in India. Agriculture continues to be a vital source of income for approximately 70% of Indian households. Given India’s agrarian economy, there are numerous incentives and benefits available to those engaged in agriculture. For instance, farmers are exempt from paying taxes on their agricultural income under Indian income tax laws. However, it’s important to note that not all income derived from agricultural land is considered agricultural income for tax purposes.

What is Agricultural Income?

According to section 2(1A) of the Income Tax Act, 1961, agricultural income is defined as follows:

Rent or revenue derived from land: This applies to land situated in India and used for agricultural purposes.

Income derived from agricultural operations: This includes basic operations such as cultivation, sowing seeds, and subsequent operations like weeding and harvesting.

Income from the sale of agricultural produce: If the produce undergoes ordinary processes to become marketable, the income from its sale is considered agricultural income.

Income derived from saplings or seedlings: Revenue generated from the sale of saplings or seedlings is considered agricultural income.

Income attributable to a farmhouse: Income from a farmhouse is considered agricultural income if certain conditions specified in section 2(1A) are met. For instance, the farmhouse should be located on agricultural land or in its immediate vicinity.

The land should not be located within the following region:

Aerial distance from municipality*

Population as per the last preceding census

Within 2 km

10,000 to 1,00,000

Within 6 km

1,00,000 to 10,00,000

Within 8 km

> INR 10,00,000

The term “municipality” encompasses various local governing bodies, including a municipal corporation, notified area committee, town area committee, town committee, and cantonment board.

It’s important to note that even if the local population is less than 10,000, the land should not be situated within the jurisdiction of the local municipality or cantonment board. This condition applies regardless of the size of the population in the area.

Non-agricultural income

As previously mentioned, certain activities related to agriculture and the income derived from them fall under the category of non-agricultural income and are subject to taxation.

Heavy Processing: When agricultural produce undergoes significant processing to become marketable, the resulting product is considered non-agricultural. Examples include tea, coffee, and rubber production. If a farmer sells processed items without engaging in agricultural or processing operations, the income is categorized as business income.

Livestock Breeding: This includes activities such as dairy farming, fishery, and poultry farming conducted on agricultural land.

Tree Plantation: Trees grown solely for timber on farmland are classified as non-agricultural income since no active agricultural business is involved in the process.

Trading: Individuals who earn income by trading agricultural produce are subject to standard taxes on their earnings.

Export: Income generated from the export of agricultural produce may be exempt from income tax if certain conditions are met.

Tax on Agricultural Income

Certainly, let’s walk through the computation for the given example:

Compute income tax on aggregate income: The taxpayer’s total income is the sum of interest income and agricultural income, which is INR 9,00,000. We’ll calculate the tax liability on this total income.

Compute income tax on the sum of the basic exemption limit plus agricultural income: The basic exemption limit for the assessment year 2023-24 is INR 2,50,000. Since the agricultural income exceeds INR 5,000, we add the basic exemption limit to the agricultural income, totaling INR 2,53,000. We’ll calculate the tax liability on this sum.

Calculate the difference between the two tax liabilities: Subtract the tax liability calculated in step 2 from the tax liability calculated in step 1.

Let’s perform the calculations to find out the tax liability for the year.

To illustrate:

Compute income tax on aggregate income: Total income (Interest income + Agricultural income) = INR 9,00,000Tax liability on total income = Tax computed as per applicable tax rates

Compute income tax on the sum of the basic exemption limit plus agricultural income: Sum of basic exemption limit and agricultural income = INR 2,53,000Tax liability on this sum = Tax computed as per applicable tax rates

Calculate the difference: Tax liability for the year = Tax liability on aggregate income – Tax liability on basic exemption limit plus agricultural income

Calculate tax on total income of INR 9,00,000

Particulars

Amount (INR)

Tax on INR 2,50,000

Nil

Tax on the second 2,50,000 @5%

12,500

Tax on remaining INR 4,00,000 @ 20%

80,000

Total Tax (A)

92,500

Calculate tax on basic exemption limit + agriculture income i.e.

Particulars

Amount (INR)

Tax on INR 2,50,000

Nil

Tax on the second INR 2,50,000 @ 5%

12,500

Tax on remaining INR 50,000 @20%

10,000

Total Tax (B)

22,500

The tax liability, in this case, will be INR 70,000 (a-b) i.e. INR 92,500 – INR 22,500

Section 54B: Capital Gain on Transfer of Land used for Agricultural Purpose

Section 54B of the Income Tax Act, 1961, is a provision that offers relief to individuals or Hindu Undivided Families (HUFs) who sell agricultural land and use the proceeds to purchase another agricultural land. Here are the key conditions to be eligible for this benefit:

Eligibility: Only individuals or HUFs can claim this benefit.

Usage for Agricultural Purposes: The agricultural land being sold and the one being purchased must be used specifically for agricultural activities.

Previous Usage: The seller or their parents must have used the land for agricultural purposes for at least two years immediately preceding the date of sale. For HUFs, any member of the HUF must fulfill this criterion.

Purchase Timeline: The new agricultural land must be purchased within two years from the date of sale. In case of compulsory acquisition, this period is calculated from the date of receipt of compensation.

Utilization of Capital Gains: The entire amount of capital gains from the sale of agricultural land must be utilized for purchasing the new agricultural land. If not fully utilized, the remaining amount will be treated as capital gains and taxed accordingly.

Holding Period: The new agricultural land cannot be sold within a period of three years from the date of its purchase to claim this benefit.

Which ITR is applicable for Agricultural Income

If the total agricultural income of the taxpayer is up to INR 5,000, it should be disclosed in the Income Tax Return (ITR) 1 form. However, if the agricultural income exceeds INR 5,000, then the taxpayer should use Form ITR 2.

Furthermore, if the income from agriculture surpasses INR 5 lakh, it must be reported separately for each agricultural land in the ‘exempt income schedule’. Additional details such as the district name with pin code, land measurement, ownership status (owned or leased), and irrigation status (irrigated or rain-fed) should also be provided. This ensures comprehensive reporting of agricultural income for taxation purposes.