Important Keyword: Income Tax Compliance, Income Tax Website, IT Notice.

Table of Contents

What is Non-Filing Monitoring System (NMS)?

The Non-Filing Monitoring System (NMS) is a system developed by the Income Tax Department to identify individuals who are required to file taxes but have not done so. Here’s how it works:

Identification of Non-filing

The NMS identifies people who are liable to file taxes—those with an annual income exceeding ₹2,50,000—but have not filed their tax returns. The system leverages several information sources to spot these non-compliant taxpayers:

AIR (Annual Information Return): Filed by financial institutions, providing details of high-value financial transactions.

CIB (Centralised Information Branch): Collects and processes data related to potential tax evaders.

TDS Statements: Details of tax deducted at source, which help in tracking the income of individuals.

Notification Process

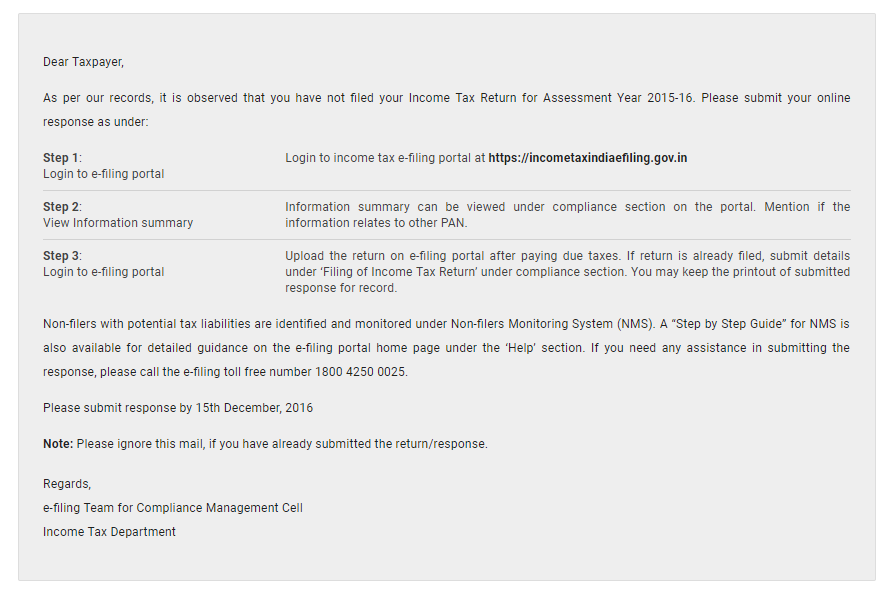

Once potential non-filers are identified, the NMS automatically sends a non-compliance email to the taxpayer’s registered email address. The Income Tax Department also sends notifications via SMS and email every year to inform non-filers of their obligation to submit their returns.

Sample email from Non-filers Monitoring System

How to respond to NMS compliance email?

Here is a step by step guide on how to deal with non-filers monitoring system email

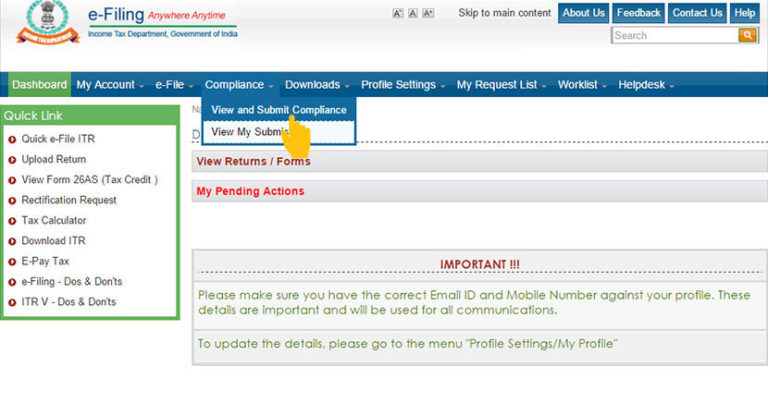

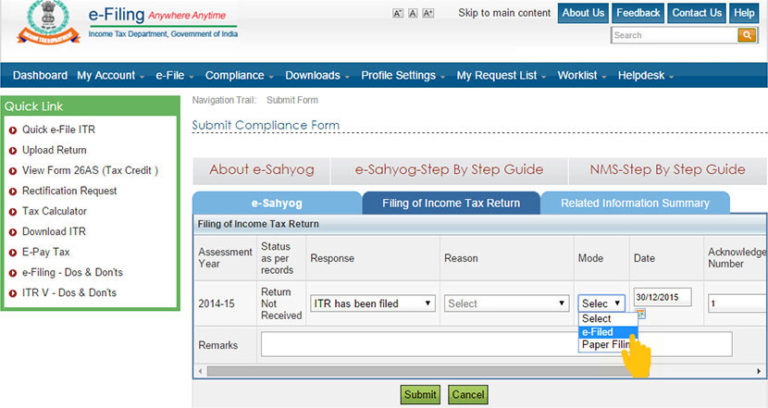

Navigate to Compliance Click on View and Submit Compliance.

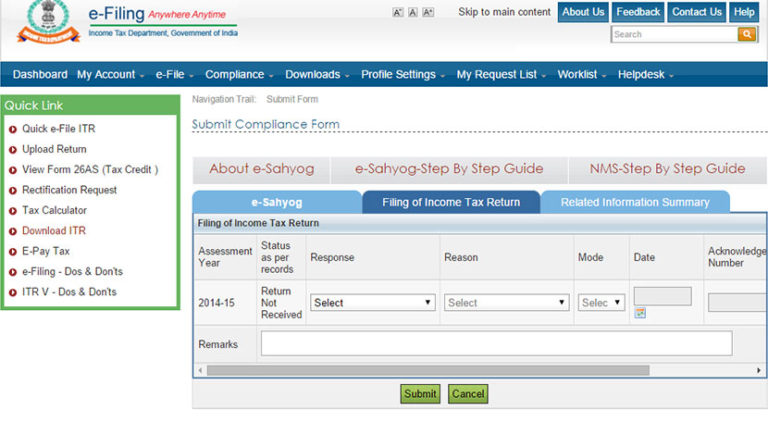

You will see the Submit Compliance Form. Navigate to Filing of Income Tax Return.

Navigate to Asssessment Year for which Return Not Received. You have two options to respond: A. ITR has been filed, B. ITR has not been filed.

If you select option (A), you need to provide: 1. Mode of filing the ITR, 2. Date of filing the ITR, 3. An acknowledgement Number.

If ITR was e-Filed, details will be prefilled automatically.

If you select option (B), you need to provide one of the following reasons: 1. Return under Preparation, 2. Business has been Closed, 3. No Taxable Income, 4. Others.

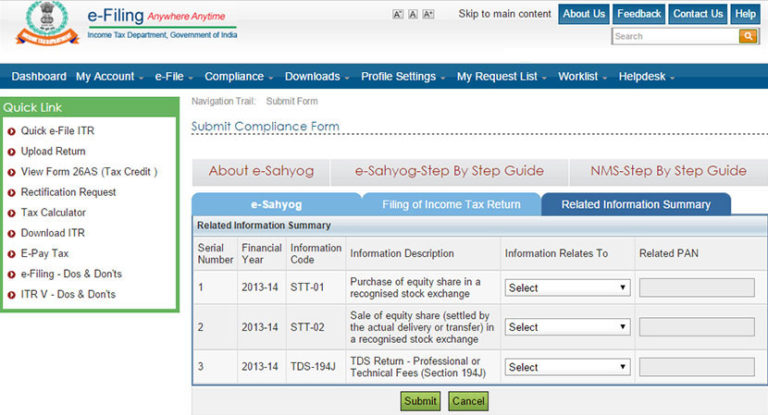

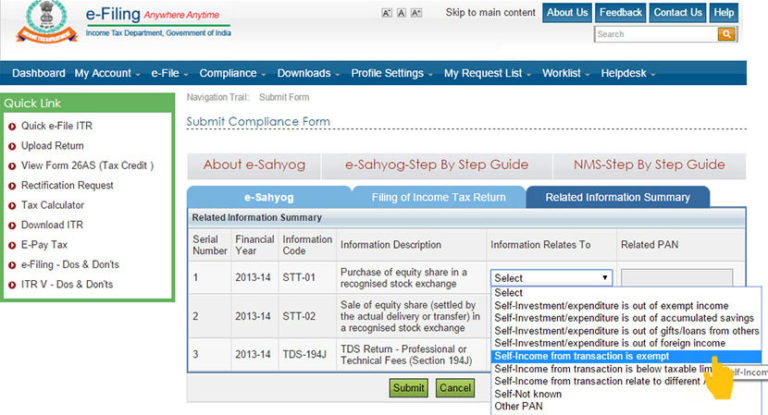

Navigate to Related Information Summary. It gives a detailed information summary.

Choose a relevant option under Information Related To against each transaction mentioned Provide additional information if required.

Following are the options available to a taxpayer under Information Relates To tab: 1. Self-Investment/ expenditure is out of exempt income 2. Self-Investment/ expenditure is out of accumulated savings 3. Self-Investment/ expenditure is out of gifts/ loans from others 4. Self-Investment/ expenditure is out of foreign income 5. Self-Income from a transaction is exempt 6. Income from a transaction is below taxable limit 7. Self-Income from transaction relate to different AY 8. Self-Not Known 9. Other PAN 10. Not Known 11. I need more information

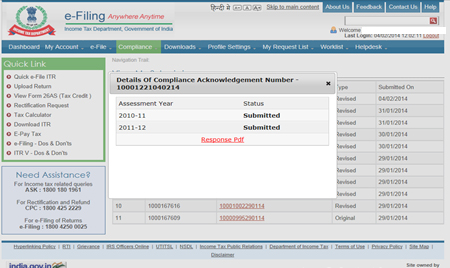

Upon submission you will see following screen. Download Response.pdf for your future reference.

Important Keyword: E-Compliance Portal, Income Tax, Income Tax Compliance, Accessing the Portal.

Table of Contents

Accessing the Portal

The Compliance Portal, administered by the Income Tax Department, serves as a specialized platform catering to various functions related to e-Verification, compliance issues, and capturing responses. It acts as a centralized hub for structured communication, fostering transparency and operational efficiency.

To access the Compliance Portal, follow these steps:

Option 1: Step 1: Directly visit the official website of the compliance portal.

Step 2: Locate and click on the Login button positioned at the top left corner to gain entry into the portal.

Once logged in, users can leverage the portal’s functionalities for addressing compliance-related matters, verifying information, and responding to queries as required.

Important Keyword: E-Verify, Income Tax Compliance, Income Tax Filing, Income Tax Returns.

Table of Contents

Responding to Filing of Income Tax Returns

The Income Tax Department (ITD) employs a notice system via the compliance portal to address non-filing of Income Tax Returns (ITRs) by identified individuals. Through an e-verification facility, the department identifies individuals who are obligated to file their ITR but have yet to do so. This proactive approach by the Compliance Portal assists both taxpayers and the department in identifying instances of non-filing of returns.

Taxpayers are required to respond on the compliance portal regarding the status of their Income Tax Returns filing. They must indicate whether the return has been filed or if it is currently in the process of being filed. This interaction between taxpayers and the Compliance Portal is crucial for ensuring compliance with tax regulations and facilitating the efficient functioning of the tax system.

By promptly responding to notices and providing accurate information on the compliance portal, taxpayers contribute to a transparent and effective tax administration process. This collaborative effort between taxpayers and tax authorities promotes accountability and strengthens the integrity of the tax system.

Steps of submitting the Income Tax Return non-filing response on compliance portal

To access the compliance portal, use your valid login credentials. Once logged in, navigate to the e-Verification tab.

In the e-Verification section, you’ll find a list of identified cases. Choose the relevant case and click on “View” to proceed.

Under the Response section, you’ll need to select one of the options from the drop-down menu.

If you choose “ITR has been filed,” provide the following details:

Mode of Filing (paper or e-Filed).

Ward and City (if filed by paper).

Date of Filing.

Acknowledgment number. Feel free to enter any remarks if necessary, then click on Submit.

Alternatively, if you select “ITR has not been filed,” you’ll need to provide a reason under the Reason section. Choose either of the following responses:

Return under preparation.

Not liable to file the return of Income. Once you’ve provided the appropriate response, click on Submit to complete the process.

Important Keyword: Compliance Portal, e-verification.

Table of Contents

View Response History

Taxpayers now have the convenience of accessing their response history through the portal. This feature allows them to track and review all responses related to specific e-Verification issues under the Related Information section.

It serves as a comprehensive platform for managing e-verification issues and capturing responses. Employing a campaign management approach, it engages taxpayers through various channels such as emails, SMS, phone calls, notices, and letters. Taxpayers are prompted to visit the portal to submit responses against identified issues.

By leveraging the portal, taxpayers can efficiently address verification concerns and ensure compliance with tax regulations. This streamlined process enhances transparency and facilitates smoother communication between taxpayers and tax authorities.

Steps to view Response History on the Compliance Portal

1. Log in to the compliance portal with valid credentials

Click on the e-Verification tab

2. Go to the Verification Issue Details section:

Go to the specific information in the Relation Information section.

3. Click the View to view the response history

As seen below:

4. You will now be able to see a list of the history of responses submitted by the taxpayer.

Click on Download PDF to download the pdf of the submitted response(s).

Important Keyword: Salary Income, Income Tax Department, E-Verify, Income Tax Compliance, Section 5(1).

Table of Contents

Tax Liability for Salary Income

Salary income under section 5(1) of the Income Tax Act encompasses various components received by an individual from their employer, including wages, annuities, pensions, gratuities, fees, commissions, perquisites, profits in lieu of salary, advance of salary, and leave encashment, among others.

However, taxpayers may encounter verification issues from the Income Tax Department (ITD) through SMS, calls, or emails for several reasons:

Non-filing of Income Tax Returns (ITRs) for the given assessment year, leading to potential tax liabilities.

Mismatch between the details provided by taxpayers and the information received by the Income Tax Department (ITD) for that assessment year.

Reporting of significant transactions during a financial year that deviate from the taxpayer’s profile.

Responding to Verification Issues: Taxpayers facing verification issues must respond promptly. The response should be submitted online through the compliance portal provided by the Income Tax Department (ITD).

Ensuring compliance with tax regulations and addressing verification issues in a timely manner is crucial for taxpayers to avoid potential penalties or discrepancies in their income tax filings. By understanding these processes, taxpayers can navigate the taxation system more effectively and contribute to a transparent and efficient tax environment.

Verification issue in the computation of tax liability from Salary Income

Code

Description

Response

A1

Total receipts as per taxpayer pertaining to the above information

Amount

A2

Less: Amount relating to another year/PAN

PAN year-wise list

A3

Less: Amount covered in other information

Amount

A4

Less: Exemption/Deduction/Expenditure/ Set off of Loss

Exemption/Deduction wise list

A5

Income/Gains/Loss (A1-A2-A3-A4)

Computed

Understanding salary components and their taxation is crucial for taxpayers.

Here’s a simplified guide to help individuals comprehend these processes:

A1-Total Receipts: This refers to the total gross salary received from the employer, including all salary components, to be mentioned as a final amount.

A2- Amount Relating to Other Year or PAN: If any part of the salary pertains to another person’s PAN or another assessment year, details should be provided in the PAN table.

A3- Amount Repeatedly Covered: Any mistakenly covered amounts should be mentioned under the Remarks section to nullify repetition.

A4- Exemption/Deduction/Expenditure/Set off of Loss: This section includes gross salary and various allowances exempted from taxation. Taxpayers need to select the correct category from the drop-down list, including exemptions related to house rent, leave travel, gratuity, perquisites, and others.

A5- Income/Gain/Loss: This section involves self-computation of taxable salary income using the formula A5=(A1-(A2+A3+A4)). If the computed income exceeds the minimum threshold of Rs. 2.5 lakh, taxpayers should file their Income Tax Returns (ITRs).

It’s essential for taxpayers to accurately declare their salary income and claim any applicable exemptions or deductions to ensure compliance with tax regulations. By understanding these concepts, individuals can navigate the taxation system more effectively and fulfill their tax obligations efficiently.