Important Keyword: Chapter VI-A, IFOS, Section 80TTB.

Table of Contents

Section 80TTB: Interest Deduction on Deposits for Senior Citizens

Senior citizens hold a pivotal role in Indian society, yet they often face substantial challenges, particularly in managing healthcare expenses and ensuring financial stability amidst fluctuating economic conditions. To address these concerns, the government has implemented various tax deductions aimed at easing the burden on senior citizens in India. One notable initiative introduced in the 2018 budget is Section 80TTB of the Income Tax Act, 1961.

Effective from the financial year 2018-19 onwards (Assessment Year 2019-20), Section 80TTB offers significant benefits to senior citizens. It specifically focuses on alleviating their financial strain by providing deductions tailored to their needs. This provision acknowledges the higher healthcare costs seniors typically incur and aims to enhance their overall financial security.

To claim a deduction under Section 80TTB of the Income Tax Act, 1961, individuals must meet specific eligibility criteria and adhere to certain rules regarding the type of interest income earned.

Eligibility Criteria:

Age Requirement: The taxpayer must be a resident individual who has attained the age of 60 years or more during the relevant financial year (AY 2023-24 in this case).

Exclusions: Non-Resident Indians (NRIs) and resident individuals below the age of 60 years cannot claim this deduction. Additionally, if the taxpayer has opted for the new tax regime, they are not eligible to claim deductions under Section 80TTB.

Threshold Limit for Deduction:

A resident senior citizen can claim a deduction of up to INR 50,000 on interest income under Section 80TTB.

If the total interest income earned from eligible deposits (like bank FDs and SCSS) is less than or equal to INR 50,000, the entire amount can be claimed as a deduction.

If the interest income exceeds INR 50,000, only a maximum of INR 50,000 can be claimed as a deduction. The excess interest income will be taxable.

Types of Eligible Interest Income:

Interest earned from Bank Deposits (including savings accounts, fixed deposits, recurring deposits).

Interest income from deposits with registered Co-operative Societies engaged in banking.

Interest income from Post Office Deposits (such as Senior Citizens Savings Scheme, NSC, Time Deposits, etc.).

Types of Ineligible Interest Income:

Interest earned on deposits held by firms, associations of persons (AOP), or body of individuals (BOI) on behalf of their partners or members.

Interest income from Bonds, Debentures, and Non-Banking Financial Companies (NBFCs).

Calculation Example: Mr. Inder, a resident senior citizen, earned the following interest income during AY 2023-24:

Interest from Bank FDs: INR 26,000

Interest from Senior Citizens Savings Scheme (SCSS): INR 32,000

Interest from Debentures: INR 3,500

Based on these earnings, Mr. Inder can claim a deduction under Section 80TTB only on the interest income from Bank FDs (INR 26,000) and SCSS (INR 32,000), totaling INR 58,000. However, since the maximum deductible limit under Section 80TTB is INR 50,000, Mr. Inder can claim INR 50,000 as a deduction, and the remaining INR 8,000 will be taxable.

Calculation of total taxable interest:

Particulars

Amount

Bank FD interest

26,000

SCSS interest

32,000

Debenture Interest

3,500

Total Interest Income

61,500

Total Interest Income Exemption u/s 80TTB

50,000

Total Taxable Interest

11,500

When reporting the deduction under Section 80TTB while filing your Income Tax Return (ITR), it’s essential to follow specific steps and understand the documentation requirements.

Steps to Claim Deduction in ITR:

Income Calculation: Start by calculating your total interest income earned during the financial year from eligible sources such as bank FDs, Senior Citizens Savings Scheme (SCSS), and similar deposits. Sum up this amount under the head “Income From Other Sources” in your ITR.

Claiming Deduction: Enter the eligible deduction amount under Section 80TTB of the Income Tax Act in the appropriate section of your ITR form (ITR 1, ITR 2, ITR 3, or ITR 4, depending on your income sources).

No Proof Submission: While filing your ITR, you are not required to submit any proof or documents supporting your claim for Section 80TTB deduction. However, it’s advisable to maintain records such as bank statements, interest certificates, and deposit documents for your own reference and in case of any future verification by tax authorities.

Supporting Documents:

Bank Statements: These documents should clearly show the interest income earned from bank FDs and savings accounts.

Interest Certificates: Issued by banks or post offices, these certificates detail the interest income earned on specific deposits like SCSS or other eligible schemes.

Deposit Documents: These include fixed deposit certificates, receipts from post office deposits, or any other relevant documents that validate your claim.

Comparison between Section 80TTA and 80TTB

Parameters

Section 80TTA

Section 80TTB

Eligibility

Individuals and HUFs (below 60 years)

Only senior citizens

Exemption Limit

Maximum INR 10,000 per year

Maximum INR 50,000 per year

Specified income

Deduction on interest from the savings account only

Deduction on interest from all kinds of deposits

Applicability for NRI’s

NRI who have a savings account (NRO) can claim a deduction u/s 80TTA

NRI’s are not eligible to claim deductions under 80TTB

Important Keyword: 80GGC, Chapter VI-A, Income Tax, Tax Benefits.

Table of Contents

Section 80GGC: Deduction on Donation to Political Parties

Political donations enable individuals to show their support for a particular party or candidate. These contributions are crucial for funding the operations of political parties. The government recognizes this and provides tax deductions on such donations. Under Section 80GGC of the Income Tax Act, taxpayers can receive tax benefits for their contributions to political parties. Therefore, if you meet the eligibility criteria, you can claim an 80GGC deduction when filing your Income Tax Return (ITR).

Eligibility Criteria for Claiming 80GGC Deduction

Individuals, Hindu Undivided Families (HUF), firms, Associations of Persons (AOP) not funded by the government, Bodies of Individuals (BOI), and artificial juridical persons not funded by the government can claim a deduction under Section 80GGC. However, companies, local authorities, and artificial juridical persons receiving government funding are not eligible for this deduction.

Eligible Entities for the Deduction

To claim the deduction under Section 80GGC, taxpayers must donate to:

A registered political party under Section 29A of the Representation of the People Act, 1951.

An electoral trust.

Section 80GGC Deduction Limits

Taxpayers can claim 100% of their contributions made through legitimate banking channels, such as internet banking, credit/debit cards, and other online payment methods, as a deduction under this section. This deduction falls under Chapter VI A, meaning the total tax deduction cannot exceed the individual’s total assessable income.

Exceptions to 80GGC Deduction

Donations in cash are not eligible under this section. Only contributions made through non-cash modes are eligible. Donations in the form of gifts or kind cannot be claimed as deductions under this section.

How to Claim the Deduction?

Eligible persons can claim an 80GGC deduction while filing their Income Tax Return (ITR), provided all conditions are met. This deduction can be claimed in ITR forms 1, 2, 3, and 4, depending on the income sources.

When filing an ITR, the taxpayer must provide:

Date of the contribution

Amounts (both in cash and through other modes)

Eligible amount of contribution

Transaction reference number for UPI transfer or cheque number/IMPS/NEFT/RTGS

IFS code of the bank

Supporting Documents Required

As proof of the donation, the political party will issue a receipt containing the name and address of the party, the amount donated, the PAN of the party, the mode of payment, and the donor’s name. These details must be submitted to the employer for inclusion in Form 16 or mentioned in the designated column when submitting tax returns.

Important Keyword: Chapter VI-A, Income from House Property, TDS.

Table of Contents

Form 12BB: Investment Declaration

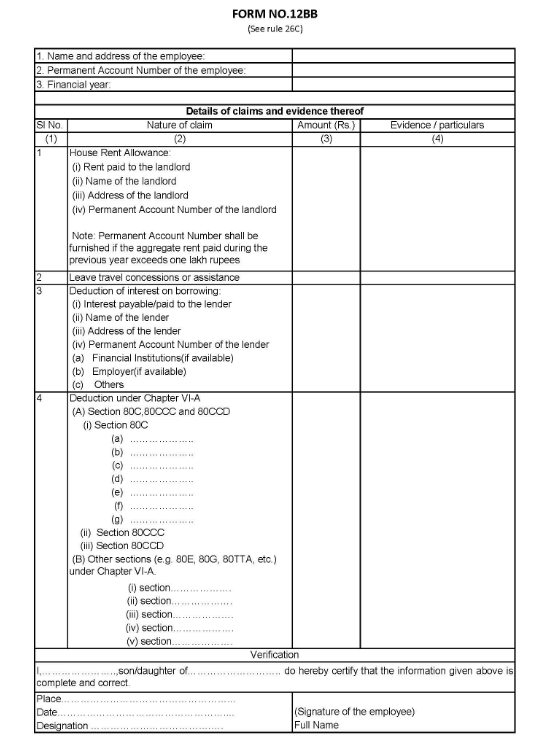

Form 12BB, also known as an Investment Declaration, holds significant importance for salaried individuals. Essentially, it entails a comprehensive disclosure of all tax-saving investments made during a specific Financial Year. Employers require this form to accurately calculate and deduct TDS on salary income. It must be submitted at the commencement of each financial year.

For instance, let’s consider Mr. Yash, who invested 3 lakhs in tax-saving schemes during FY 2019-20. He is required to file his Form 12BB, disclosing all investment details to his employer between April 1, 2019, and June 30, 2019. Subsequently, he can submit evidence of these investments between January 1, 2020, and March 31, 2020. This practice ensures precise TDS deduction and is advisable for maintaining accurate financial records.

Sample Form 12BB – Investment Declaration

Supporting Documents

Include essential details such as:

Personal Information: Name, Address, PAN, and Designation of the employee.

Current Financial Year.

Details regarding:

House Rent Allowance (HRA)

Leave Travel Concession or Assistance (LTA)

Deduction of Interest on Borrowing

Deduction under Chapter VI-A

Additional Information: Place, Date, and Signature.

These documents are crucial for accurately declaring tax-saving investments and allowances to the employer for appropriate TDS calculation on salary income.

Important Keyword: Chapter VI-A, Form 12BB, Income from House Property, TDS.

Table of Contents

How to fill Form 12BB?

All salaried taxpayers are required to complete Form 12BB. This form must be submitted to their employer at the start of each financial year to facilitate accurate Tax Deducted at Source (TDS) deductions. Form 12BB serves as a declaration of all tax-saving investments made by the employee during the relevant financial year. By disclosing these investments, employees ensure that their TDS deductions are calculated correctly in line with their eligible tax-saving investments.

Steps to Fill Form 12BB

To download a sample Form 12BB, you can visit the Income Tax Department website.

Personal Details:

Name: [Your Name]

Address: [Your Address]

PAN: [Your PAN Number]

Financial Year: 2020-2021

House Rent Allowance (HRA) Details:

If incurring rental expenses for work, include details here.

Leave Travel Allowance (LTA) Details:

Include details of LTA if applicable.

Interest on Loan for Borrowings:

Enter details of interest on EMI of home loans for the current financial year.

Benefits up to INR 2,00,000 for self-occupied property and no limit for rented property.

Chapter VI-A Deductions:

Add details of tax-deductible investments and deductions under various sections such as 80C, 80CCD (1B), 80D, 80DD, 80E, 80G, etc.

Who needs to Fill Form 12BB?

Since 1st June 2016, it’s mandatory for every salaried taxpayer to submit Form 12BB. Along with the form, you need to provide proofs/evidence supporting your investments. This helps in reducing your taxable income and ensures accurate TDS deduction by your employer from your salary.

However, if you fail to file Form 12BB, your employer might deduct excess TDS from your salary. Don’t worry though, you can claim back this excess TDS while filing your Income Tax returns. It’s important to ensure timely submission of Form 12BB to avoid unnecessary deductions and streamline your tax obligations.

Important Keyword: AMT, Business and Profession Income, Chapter VI-A, Slab Rates.

Table of Contents

AMT – Alternative Minimum Tax under Section 115JC

The Income Tax Department introduced the Alternate Minimum Tax (AMT) as a measure to ensure that taxpayers, excluding companies, contribute a minimum amount of tax, particularly those who exploited incentives and deductions excessively, resulting in zero tax liability. To curb misuse and promote fair taxation, the government implemented Minimum Alternate Tax (MAT) for companies and AMT for other taxpayers.

AMT aims to collect a minimum level of tax from eligible taxpayers, with provisions allowing for the carry-forward of AMT credits to offset future tax liabilities.

Applicability of Alternative Minimum Tax:

Individual, Hindu Undivided Family (HUF), Association of Persons (AOP), or Body of Individuals (BOI) with adjusted total income exceeding INR 20 lakhs.

Any taxpayer, excluding companies, regardless of total income.

AMT provisions apply to eligible taxpayers under the following conditions:

Claiming deductions under Sections 80H to 80RRB, excluding Section 80P.

Claiming deductions under Section 35AD.

Claiming deductions under Section 10AA.

AMT Rate & Adjusted Total Income

Rate of Alternative Minimum Tax is 18.5% of the Adjusted Total income. In addition to this, surcharge and cess are applicable. Calculate the adjusted total income in the following manner:

Particulars

Amount (INR)

Taxable Income

XXXX

Add

Deduction claimed u/s 80H to 80RRB (except 80P)

XXXX

Add

Deduction claimed u/s 35AD reduced by regular depreciation allowed as per Section 32

XXXX

Add

Deduction claimed u/s 10AA

XXXX

Adjusted Total Income

XXXX

AMT – 18.5% of Adjusted Total Income

XXXX

If the provisions of Alternative Minimum Tax (AMT) apply to a taxpayer, the tax liability would be higher of the following:

Tax Liability as per the normal provisions of the Income Tax Act:

Calculate the Total Income of the taxpayer from all sources of income. After claiming deductions under Chapter VI-A, compute the Tax Liability on the Total Income as per the applicable slab rates.

Tax Liability under AMT:

Calculate the Adjusted Total Income by adding back the deductions claimed under specified sections. Apply the AMT rate of 18.5% to the Adjusted Total Income. Additionally, surcharge and cess, if applicable, are added to the AMT amount for final computation. Compare the tax liability calculated under both methods, and the higher amount will be the taxpayer’s tax liability for that financial year.

This ensures that if the tax liability computed under the normal provisions of the Income Tax Act is lower than the tax liability under AMT, the taxpayer will be required to pay tax as per the AMT provisions, ensuring a minimum level of tax payment.

Scenario Analysis:

Samir’s Taxable Income and AMT applicability.

Aryan Enterprises’ AMT Credit and utilization.

Samir’s Case:

Taxable Income: INR 18,00,000.

Deduction under Section 80QQB: INR 3,00,000.

Adjusted Total Income: INR 21,00,000.

AMT Applicability: Adjusted Total Income > INR 20 lacs.

Tax Liability Calculation:

Normal Provisions: INR 3,66,600.

AMT Provisions: INR 4,04,040.

Final Tax Liability: Higher of the two: INR 4,04,040.

AMT Credit Utilization:

Aryan Enterprises’ FY 2019-20: Normal Tax – INR 15,00,000, AMT – INR 18,00,000.

Carry Forward AMT Credit: INR 3,00,000.

FY 2020-21: Normal Tax – INR 10,00,000, AMT – INR 9,00,000.

Utilized AMT Credit: INR 1,00,000, Remaining: INR 2,00,000.

CA Report:

Obtain Form 29C from a Chartered Accountant.

Certification of Adjusted Total Income and AMT compliance.