Important Keyword: Income Tax, IT Notice, Notice u/s 148.

Table of Contents

Section 148: Income Escaping Assessment

The taxes paid by individuals are vital for funding public services. However, there are instances where taxpayers might either intentionally or unintentionally fail to report certain portions of their income when filing their taxes. In response to this, tax authorities conduct thorough examinations to ensure accurate reporting of all income sources. In such situations, the Assessing Officer issues a notice under Section 148 for ‘Income Escapement Assessment’. The objective of this assessment is to uncover any concealed income, whether it was intentionally hidden or overlooked due to inadvertence.

Section 148 of the Income Tax Act

If upon reviewing the filed return, the Assessing Officer (AO) harbors doubts regarding the completeness of income disclosure by the taxpayer, they can initiate further assessment proceedings by issuing a notice under section 148.

In accordance with the Finance Act 2022, section 148A was introduced. In compliance with this section, the AO must conduct an inquiry and grant the taxpayer an opportunity to present their explanation before issuing a notice under section 148. The taxpayer must be allowed to provide their explanation within a timeframe of 7 days, which can be extended for up to 30 days.

The issuance of a Notice under Section 148 is subject to various conditions and terms as follows:

The AO must have a valid reason to believe that taxable income has escaped assessment, supported by substantial evidence. Mere suspicion without evidence cannot be the basis for such a notice.

The AO must provide the reasons in writing before issuing the notice under section 148. A mere change of opinion cannot constitute a reason to believe.

The AO cannot issue a notice based on information provided by the taxpayer during the assessment.

The AO can only issue a notice if they have received new information and not discovered it themselves by reading.

The AO can issue a notice if previously disclosed relevant information comes to notice, even at a later time.

Furthermore, notice under section 148 can only be issued if the following conditions are satisfied:

The taxpayer failed to file the return in response to the notice under section 142.

The taxpayer filed the return under Section 139.

The taxpayer is providing complete and accurate information for completing the assessment of the relevant Assessment Year.

The time limit for issuing a notice for income escaping assessment is provided under section 149 of the Income Tax Act. According to Section 149:

The notice can be issued within 4 years from the end of the relevant assessment year.

The AO can issue a notice up to 10 years from the end of the relevant assessment year if specific conditions are met.

A notice for income escaping assessment related to assets located outside India can be issued within 16 years from the end of the relevant Assessment Year.

As for who can issue a notice under Section 148:

An AO above the rank of Assistant Commissioner or Deputy Commissioner can issue a notice, provided the Joint Commissioner is convinced, with recorded justifications, that it is an appropriate case.

The AO cannot issue a notice after 4 years from the end of the relevant assessment year, but higher authorities can issue it even after this period if valid reasons are found.

Regarding replying to the notice under Section 148:

Upon receiving the notice, the taxpayer should review the recorded reasons for issuing the notice. If these reasons are not provided, the taxpayer must request the AO to furnish a copy of the recorded reasons.

If the taxpayer agrees with the reasons given by the AO, they must respond within the stipulated time frame by either filing the requested return or providing the documents and information as requested.

The taxpayer can dispute the validity of the notice before the AO or higher authorities if the notice is found to be invalid or if the reasons for initiating the assessment under section 147 are deemed inadequate.

If the authority’s decision favors the taxpayer, assessment procedures can be suspended. However, if the authorities rule against the taxpayer, the AO can proceed with the reassessment.

Consequences of not responding to notice

In cases where a taxpayer fails to respond to the notice issued under section 148, the Assessing Officer (AO) has the authority to conduct the assessment based on the available information. This means they can estimate the taxpayer’s income and assess it to the best of their judgment under section 144 of the Income Tax Act.

If taxpayers disagree with the assessment made by the AO, they have the option to file an appeal. The appeal can be filed with either the Commissioner of Income Tax (Appeals) or the Income Tax Appellate Tribunal (ITAT). These are the next levels of authority where taxpayers can contest the assessment and present their case for review.

Important Keyword: Income Tax, IT Notice, Notice under Section 156.

Table of Contents

Section 156: Notice of Demand

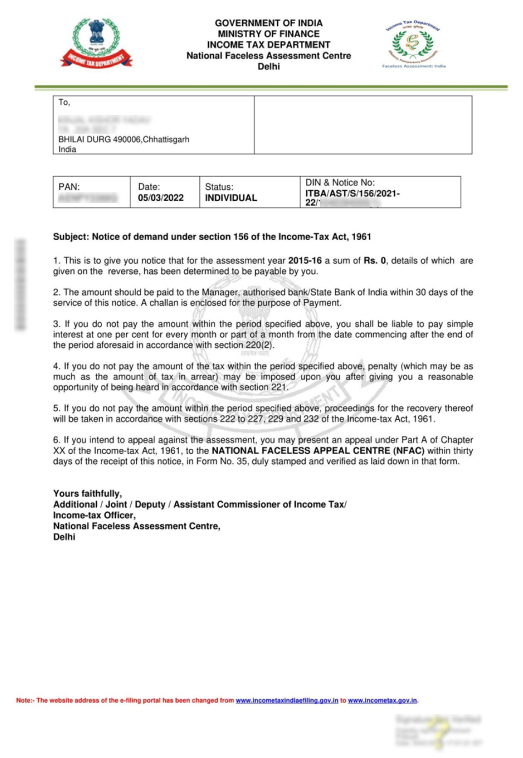

After the completion of the assessment or re-assessment process, the Income Tax Department undertakes the crucial task of evaluating whether any additional tax liability is owed by the taxpayer. If such an outstanding liability exists, the department initiates the process by issuing a demand notice as per section 156 of the Income Tax Act. This notice serves to inform the taxpayer of the total amount due, comprising of various components such as interest, penalties, fines, and any other applicable charges. Additionally, the notice stipulates a specific timeframe within which the taxpayer is required to settle the outstanding amount.

Notice for Outstanding Demand under Section 156?

When an order is issued under the provisions of the Income Tax Act, and it entails an outstanding liability, the Income Tax Department issues a notice under section 156 to the taxpayer. This notice encompasses demands related to various sections of the Act, such as section 143(1), 200A(1), 206CB(1), among others. Any notice specifying a sum payable under these sections is regarded as a Demand Notice under section 156. The taxpayer is obligated to remit the specified amount within 30 days of receiving the notice.

Sample Notice under section 156

How to Respond to Outstanding Tax Demand Notice?

For submitting a response to outstanding demand, the taxpayer can follow below-mentioned steps:

Log in to the e-Filing Portal Log in to the e-Filing portal. Navigate to Pending Actions > Response to Outstanding Demand to view a list of your outstanding demands from the dashboard.

If you agree pay the demand amounts before submitting a response. Click on Pay Now to make payment of outstanding demand.

Submit Response If the taxpayer has not paid the demand or disagrees with the demand then they can submit their response accordingly.

Further, the taxpayer has the following options available for submitting a response to the demand notice issued u/s 156.

Agree with demand.

Fully disagree with demand.

Partially disagree with demand.

Option 1: Agree with Demand

Part A- Demand is correct but payment is pending. If you agree with the demand notice, you can select the Demand is Correct option. Moreover, you get an opportunity to pay the dues from here only by selecting Not Paid Yet option. Once the payment is done, the response to the demand will be submitted automatically.

Part B: The demand is correct and amounts are already paid. On the Response to Outstanding Amount page, select the Demand is Correct option and the disclaimer. Then click on the checkbox with Yes, Already paid and Challan has CIN, and Click on Add Challan Details.

Here, input the challan details. After entering the details, upload a copy of the challan (PDF). Once you save the challan details, the system will display a success message along with the transaction ID on the next tab.

Option 2: Fully Disagree with demand.

If you disagree with the demand notice, select Disagree with the demand (Either in full or in part) option and click on Add Reasons.

Then, select the reason(s) for your disagreement from the options and click Apply. (You can select one or more options)

After selecting the appropriate reasons for your disagreement, select each reason you listed on the Response to Outstanding Amount page and enter the appropriate explanation for disagrrement. Once the explanation is saved, submit the response.

Option 3: Partially disagree with Demand.

If a taxpayer believes that the outstanding demand is only partially correct, they have the option to submit reasons for their disagreement. In such cases, the taxpayer is required to make payment for the portion of the amount with which they agree. Once the payment is successfully made, the system will prompt the taxpayer to proceed to the Response to Outstanding Amount page. Here, they can submit their response. Upon successful submission, the system will display a confirmation message along with a Transaction ID.

Time Limit to Respond

The taxpayer must settle the outstanding demand within 30 days from the date of service of the notice. However, in certain instances, the assessing officers may reduce this period to 30 days if they deem it detrimental for the department to allow a longer period for payment, with prior approval from the joint commissioner.

Furthermore, taxpayers can apply for an extension of the payment period or request to make payments in installments. However, such applications must be made before the end of the initial 30-day period.

Consequences of Delay

Interest under section 220(2): Interest is levied at a rate of 1% per month or part of the month after the expiration of the initial 30-day period. This interest is payable by the taxpayer, even if the assessing officer has approved an extension of the payment period.

Penalty under section 221: The assessing officer has the authority to impose a penalty of up to the amount of the demand specified in the outstanding demand notice. However, the taxpayer must be given a reasonable opportunity to be heard. If the taxpayer can demonstrate that the default occurred due to genuine reasons, no penalty will be imposed.

Important Keyword: Income Tax, PAN & Aadhaar, PAN Status, TIN NSDL, Track PAN.

Table of Contents

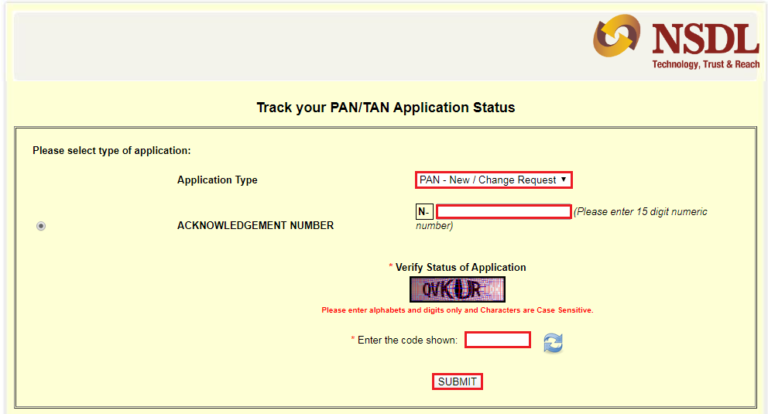

Check PAN Card Application Status on NSDL

The Permanent Account Number (PAN) is a unique 10-digit alphanumeric identifier issued by the Income Tax Department (ITD) of India. For those who have applied for a PAN card, it’s crucial to know how to check the status of your application. Here is a straightforward guide to help you track your PAN card application status on the Tax Information Network- National Securities Depository Limited portal.

The TIN-NSDL e-Gov portal offers a convenient way to update or correct details in your PAN card. After making the necessary changes, you will receive a new PAN card reflecting all the updated information as requested.

Steps to Check PAN Card Status on National Securities Depository Limited

Follow steps below to monitor the PAN status of the application that you have applied using TIN-NSDL Portal.

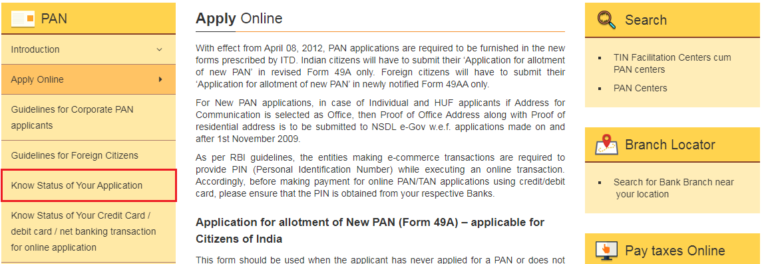

Visit the TIN-National Securities Depository Limited portal and click on PAN Navigate to Services > PAN option from the dashboard on the TIN-NSDL portal.

Select the appropriate option Navigate to “Know Status of Your Application” option to check your PAN status.

Choose following options Select the “Application Type” from the drop-down list and enter the “Acknowledgment Number.”

Enter Captcha Enter the captcha code from the given image.

In case you applied via UTITSL portal, you can check your PAN card application status there.

Important Keyword: Form 16, Form 26AS, Income Tax, ITR Forms & Documents, ITR-1, Salary Income.

Table of Contents

AY 2021-22 ITR-1 SAHAJ Form – Salaried Individuals

ITR-1, also known as Sahaj, is the simplest one-page Income Tax Return Form tailored for individuals with income from Salary/Pension, One House Property, and income from other sources. However, there are certain criteria to consider before determining eligibility for filing ITR 1.

Who Can File ITR-1 Form?

Any individual whose total income does not exceed INR 50 lakh and includes:

Salary/Pension Income.

Income from one House Property (excluding brought forward losses from previous years).

Income from Other Sources (excluding winnings from Lottery and Income from racehorses).

If the income of a spouse or minor child is clubbed with the taxpayer’s income, they can file ITR 1 only if their clubbed incomes fall within the above categories.

Who Cannot File ITR-1 Form?

Non-Resident Indians (NRIs)

Individuals with total income including:

Income from multiple House Properties

Income from winnings from lottery or income from racehorses

Capital Gains Income (short-term and long-term Capital Gains from the sale of house, plot, shares, etc.)

Agricultural income exceeding INR 5000/-

Income from Business and Profession

Resident individuals having any asset (including financial interest in any entity) located outside India or signing authority in any account located outside India

Individuals claiming relief of Foreign Tax paid or Double Taxation Relief under section 90/90A/91.

List of Documents Required to File ITR 1:

Essential Documents:

PAN (Permanent Account Number)

Aadhaar Number

Bank Account Details

Form 26AS

Form 16

AIS – Annual Information Statement

Details of original return if filing revised return

Details of notice if filing in response to a notice

Additional Documents:

For Salary Income:

Form-16 or Salary slips received from your employer

Pension statement/passbook.

For House/Property Income:

Address of the property

Co-owner details (if applicable)

Interest certificates/Repayment certificate from a bank (for property loan)

Rent Agreement (for let-out property)

For Other Sources:

Savings/Current Account Statements/Passbook

Interest Certificates for deposits/bonds/NSC

PPF Account Statement/Passbook

Dividend warrants/counterfoils

Rent Agreement (for let-out machinery)

Details about receipts of any other income

Income Tax Return Form – ITR 1

Here are the major changes in ITR 1 for Assessment Years 2021-22, 2020-21, and 2019-20:

For AY 2021-22:

Option to Choose Tax Regime: Taxpayers can opt between the old and new tax regimes.

Quarterly Breakdown for Dividend Income: Dividend income must be reported with quarterly breakdowns for accurate calculation of interest under Section 234C.

For AY 2020-21:

Expanded Eligibility Criteria: Individuals meeting specific criteria like cash deposits above INR 1 crore, foreign travel expenses above INR 2 lakh, or electricity expenses above INR 1 lakh must file ITR 1.

Continued Basic Criteria: Individuals with income from salaries, one house property, other income, and total income up to INR 50 lakh remain eligible.

Single Property Ownership: Resident individuals owning a single property in joint ownership can also file ITR 1 if their total income is up to INR 50 lakh.

Disclosure of Tax-Saving Investments: Taxpayers must disclose investments, deposits, or payments towards tax-saving made from April 1, 2020, to June 30, 2020.

For AY 2019-20:

Exclusion of Certain Individuals: ITR 1 is not applicable to individuals who are directors of a company or have invested in unlisted equity shares.

Introduction of Pensioners Checkbox: Under Part A, a ‘Pensioners’ checkbox is introduced under the ‘Nature of employment’ section.

Segregation of Returns: Returns filed under section segregated between normal filing and filing in response to notices.

Deduction Segregation: Deductions under salary segregated into standard deduction, entertainment allowance, and professional tax.

Detailed Income Information: Taxpayers required to provide income-wise detailed information under ‘Income from other sources’.

Family Pension Deduction: Introduction of a separate column for deduction under Section 57(iia) for family pension income.

Deemed Let Out Property Option: Inclusion of ‘Deemed to be let out property’ option under ‘Income from house property’.

Section 80TTB for Senior Citizens: Inclusion of Section 80TTB column for senior citizens.

Important Keyword: Form 15G, Form 15H, Income Tax, ITR Forms & Documents, optimized, TDS.

Table of Contents

What is Form 15G/Form 15H?

Form 15G/15H serves the purpose of ensuring that TDS is not deducted from your income if you meet specific conditions. These forms can be submitted to the deductor responsible for deducting TDS on your income.

A prime example of their use is with banks. Banks typically deduct TDS at a rate of 10% if your interest income from deposits exceeds INR 10,000 (INR 50,000 for senior citizens). If your total income is not taxable, you can submit Form 15G/15H to banks to prevent them from deducting TDS from your interest income. Some banks even allow the online submission of these forms through their websites.

Form 15H is designed for senior citizens aged 60 years or above, while Form 15G is for non-senior citizens. These forms need to be filed at the beginning of each financial year.

What are the conditions for filing Form 15G/ Form 15H?

The conditions for filing Form 15G are as follows:

Your age is less than 60 years.

You are a Resident Individual or HUF.

Tax calculated on your Total Income is zero.

Total Interest income is less than the basic exemption limit of that particular year.

Similarly, for filing Form 15H, the conditions are the same as above, except the individual’s age should be 60 years or above.

Age of the individual

Basic Exemption Limit (INR)

Below 60

2,50,000

Between 60 and 80

3,00,000

More than 80

5,00,000

Let’s take an example to understand better:

Particulars

Anjana

Rahul

Gautam

Pravin

Age

25

50

70

65

Residential Status

Resident of India

Resident of India

Non-Resident of India

Resident of India

Salary Income / Pension Income

2,70,000

0

0

1,50,000

Interest Income

10,000

2,60,000

85,000

20,000

Total Income

2,80,000

2,60,000

85,000

1,70,000

Deduction under Section 80

40,000

50,000

0

0

Total Taxable Income

2,40,000

2,10,000

85,000

1,70,000

Basic Exemption Limit

2,50,000

2,50,000

3,00,000

3,00,000

Form 15G/15H eligibility

Yes

No

No

Yes

Reason

Anjana can submit Form 15G Since the tax calculated is zero and interest income is less than the basic exemption limit

Rahul cannot file Form 15G. Even Though the tax calculated is zero because his interest income exceeds the basic exemption limit (INR 2,50,000)

Gautam cannot file Form 15H since he is not a resident Indian

Pravin can file Form 15H since his tax calculated is zero and interest income is less than the basic exemption limit (INR 3,00,000)

How to file Form 15G & Form 15H?

Form 15G/15H is utilized to ensure that TDS is not deducted from your income. If your tax liability for the year is zero, you can file these forms with the deductor responsible for TDS deduction. They can be filed either physically or online through the following methods:

Physical Submission:

Download Form 15G/15H, fill it out, and submit it to the deductor in paper form.

Online Submission:

Visit the website of the deductor (e.g., Bank’s website).

Log in to your account, fill out Form 15G/15H, and submit it online.

Details required for filing Form 15G/15H include PAN, residential status, address details, contact information, estimated income details, and details of previously filed Form 15G/15H.

Form 15G/15H should be submitted for the following income sources when TDS is deducted:

EPF Withdrawal: If withdrawing from the EPF account before completing 5 years of continuous service, and the withdrawal amount exceeds INR 50,000, Form 15G/15H can prevent TDS deduction.

Rent: If rental income for the year exceeds INR 2,40,000, TDS is deducted by the tenant. However, if the total income, including rent, is not taxable, Form 15G/15H can be submitted to the tenant to avoid TDS deduction.

Interest Income from FDs with Banks/Post Office: If total income, including interest from deposits, is not taxable, Form 15G/15H can be submitted to the Banks/Post office to prevent TDS deduction.

Corporate Bonds: If interest income from corporate bonds exceeds INR 5000, TDS is deducted. Form 15G/15H can be submitted to the issuer to avoid TDS deduction.

Insurance Commission: Insurance agents can submit Form 15G/15H to avoid TDS deduction if tax on their total income is zero.

Dividend Income: From FY 2020-21, TDS @ 10% will be deducted on dividend income exceeding INR 5,000. Traders can submit Form 15G/15H if tax on their total income is zero to avoid TDS deduction.